Table of Contents

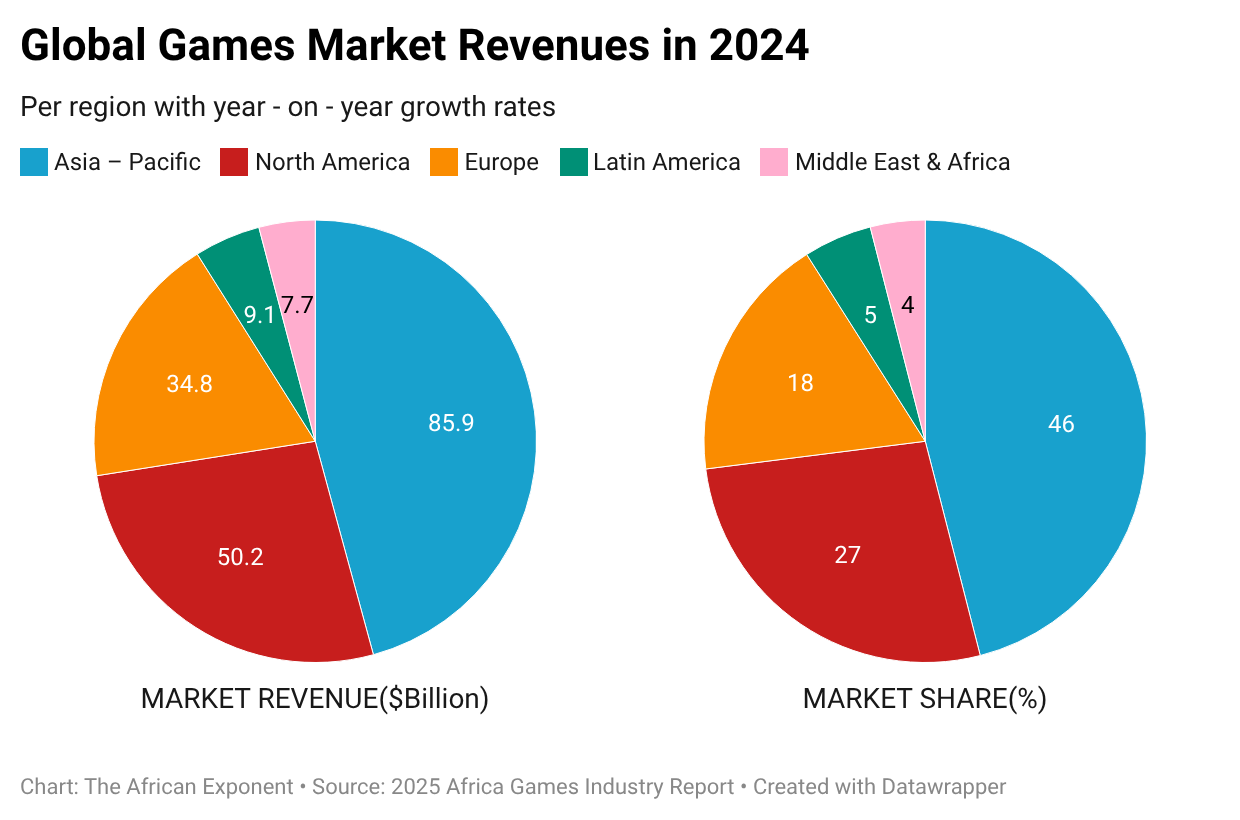

Africa’s gaming audience is expanding rapidly, but the continent’s developer economy is struggling to capture the full value of that growth. According to the Africa Games Industry Report 2025, mobile gaming generated more than $200 million in revenue across five key African markets in 2024, reflecting strong consumer demand. Yet 85% of African game studios earn less than $100,000 annually, highlighting a structural disconnect between player engagement and developer income.

This gap is not primarily about demand. Instead, it reflects weaknesses in the monetization infrastructure connecting African gamers to developers’ bank accounts. Between the moments a player downloads a game and the moment a studio receives revenue sits a complex chain of intermediaries: platform operators, payment processors, and regional distributors.

Understanding how these layers function, and who controls them is critical to understanding where Africa’s gaming economy generates real financial value, and where the revenue ends up.

What are the Five Key Markets Driving Africa’s Mobile Gaming Revenue?

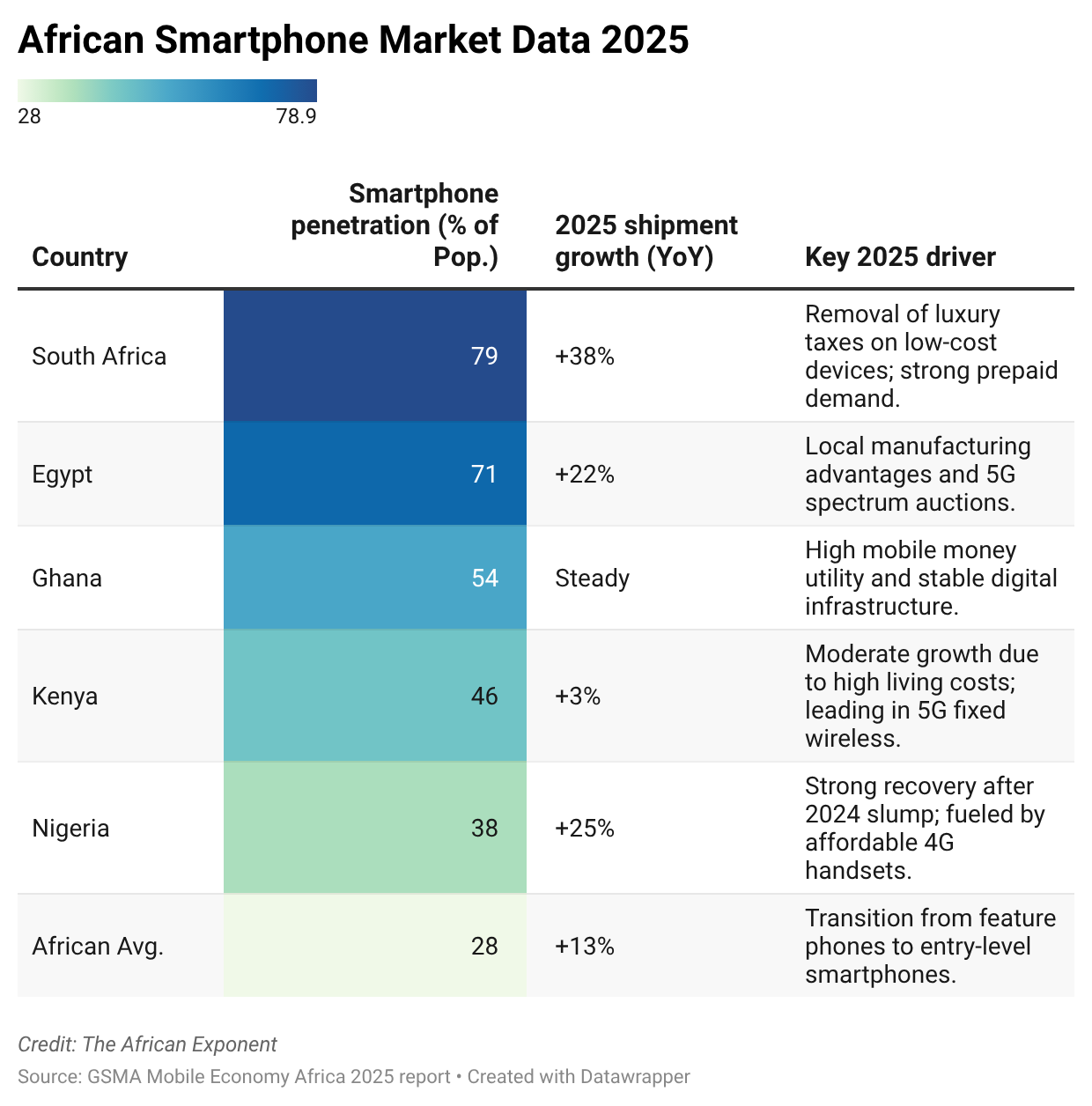

Much of Africa’s mobile gaming revenue is concentrated in a handful of relatively mature digital markets. According to the report, the five key African mobile gaming markets in 2024/2025 were South Africa, Nigeria, Kenya, Egypt, and Ghana.

These countries combine relatively high smartphone penetration, expanding mobile broadband networks, and growing fintech ecosystems that support in-app purchases. South Africa and Egypt benefit from stronger card-based payment systems and larger digital economies, while Nigeria and Kenya rely more heavily on mobile-first payments and large youth populations driving game downloads. Ghana, though smaller, has emerged as a fast-growing mobile gaming market due to improving connectivity and digital payments adoption.

Together, these five markets form the core of Africa’s current gaming economy, accounting for the majority of mobile gaming revenues while also serving as testing grounds for monetization strategies that could later expand across the continent.

The Middleware Layer: What Sits Between the Developer and the Gamer?

In mature gaming markets, monetization follows a predictable pipeline of discovery, integrated purchase, and revenue collection. In Africa, however, this process is significantly more fragmented. While mobile games account for 90% of all industry revenue on the continent, the lack of seamless billing means much of this value remains trapped. To bridge this "conversion gap," developers must navigate complex intermediaries where payment infrastructure, distribution, and licensing typically consume 40% to 60% of gross revenue. These regional costs, far exceeding the 15–30% standard of global app stores, drastically reduce net margins, making the "cost of reach" the single greatest hurdle to scaling digital content.

Most games are distributed through platforms such as Google Play and the Apple App Store, which control visibility, distribution, and payments. Whilst Africans have access to these, limited banking access means many players cannot use card-based systems, making mobile money services like M-Pesa and MTN MoMo — which is rapidly gaining acceptance in many parts of Africa, critical bridges for digital purchases.

Regional publishers are the essential middleware of Africa’s gaming economy, managing localization, marketing, and cross-border distribution. A definitive example is Carry1st, which partnered with Riot Games to expand titles like Valorant into South Africa and Nigeria. By integrating its "Pay1st" platform, Carry1st enabled players to use local methods like 1Voucher and mobile money—options not natively supported by global clients. By handling everything from IP licensing to local server hosting, these partners provide the critical infrastructure that transforms global titles into localized, revenue-generating assets.

How Do Payments and Conversion Stand as a Barrier in Africa’s Gaming Revenue?

While the continent’s gaming ecosystem is overwhelmingly mobile-first, with mobile games now accounting for 90% of all industry revenue, fragmented payment systems remain one of the most significant barriers between African gamers and developer growth. Many players lack access to the banking tools typically required for digital purchases. According to the GSMA State of the Industry Report on Mobile Money 2025, sub-Saharan Africa has around 1.1 billion registered mobile money accounts, yet credit card penetration remains relatively low. So, because global app stores such as Google Play and the Apple App Store rely heavily on card-based payments in many markets, there is a limitation on how easily players can complete in-game purchases.

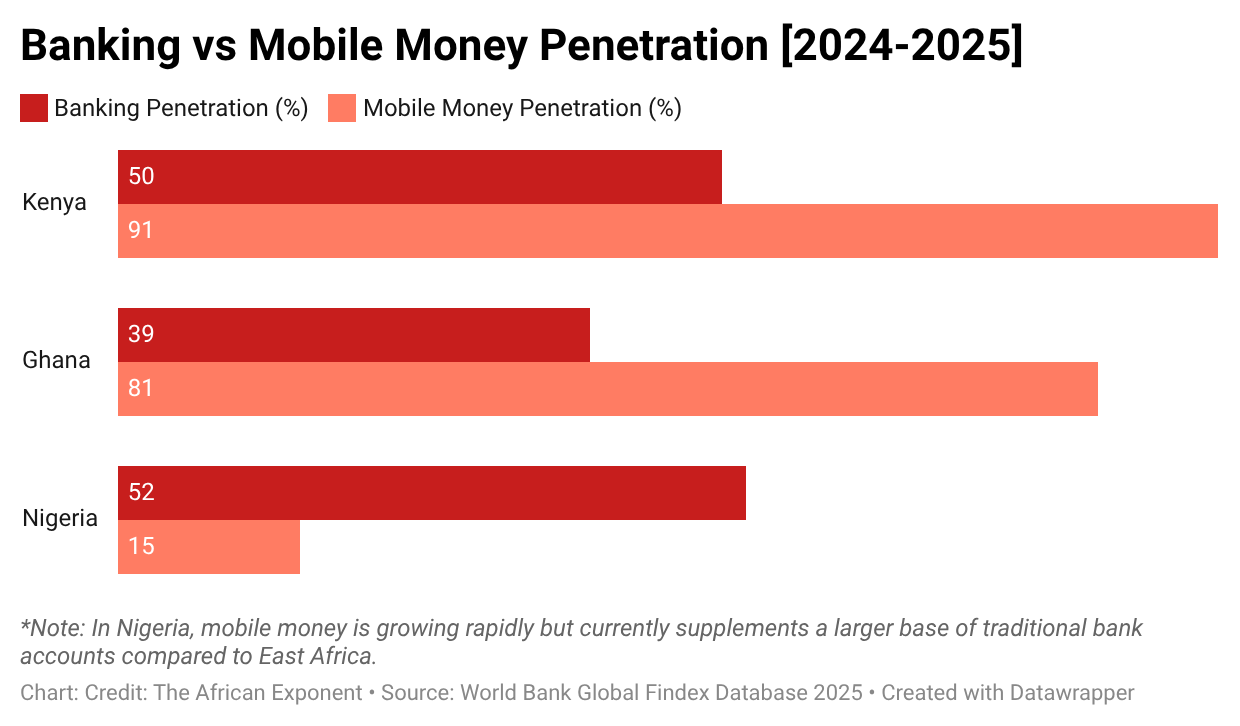

This shift results in a profound "conversion gap": while millions of users download and play games, the reliance on traditional banking for in-app purchases creates a systemic barrier to monetization. In key markets like Kenya and Ghana, mobile money penetration (91% and 81% respectively) dwarfs traditional banking access, which sits significantly lower at 50% and 39%. Because global app store infrastructures are built primarily for credit card economies, they fail to reach the majority of African players who are "banked" only through their mobile wallets. This misalignment ensures that even as engagement stays high, the payment infrastructure required for microtransactions remains fundamentally disconnected from the continent’s primary financial reality.

Across the continent, mobile gamers can easily install titles through app stores but often face friction when attempting to make purchases that require international cards. A player may actively engage with a game for weeks yet abandon a purchase simply because the payment system requires a credit or debit card they do not possess. This disconnect between player engagement and payment capability helps explain why Africa can have millions of gamers but relatively modest in-app purchase revenues compared with other regions.

How is Cross-Border Distribution a Challenge to Africa’s Gaming Revenue?

Even when studios solve payment challenges domestically, scaling across African markets remains difficult. The Africa Games Industry Report 2025 finds that 52% of African studios earn all their revenue locally, limiting growth and overexposing game studios to the aforementioned infrastructure gaps in their markets.

Expanding regionally involves adapting pricing, integrating local payment methods, and funding marketing campaigns, even when distributing through platforms like Google Play or the Apple App Store. App store commissions, usually between 20% to 30% to the studios or developers, and currency volatility further compress margins.

For example, Maliyo Games struggled to scale Djogo Striker Legends into East Africa; despite Google Play distribution, it had to compromise its profit margin by 40%-60%, by partnering with a Spanish digital monetization company, Telecoming, to distribute the mobile game across multiple African markets. Due to the partnership, Maliyo bypassed payment barriers by allowing users to pay via mobile airtime. While this "aggregator" model requires significant revenue sharing with tech partners and mobile operators, it provided the essential scale to transform a local hit into a pan-African commercial success.

Does Intellectual Property Licensing and Content Monetization Also Contribute to the Revenue Gap?

Yes. Limited intellectual property (IP) licensing and weak content monetization channels are another factor widening the revenue gap in Africa’s gaming sector. While many African studios create culturally distinctive games, the ecosystem needed to turn those titles into scalable franchises through licensing, merchandise, or cross-media partnerships remains underdeveloped. Cameroon-based Kiro'o Games illustrates this conundrum.

Kiro’o built Aurion: Legacy of the Kori-Odan around African mythology and political storytelling, positioning it as a broader narrative universe rather than a single game. Yet monetizing that IP beyond game sales has been limited by the absence of strong regional publishing and entertainment partnerships.

Similarly, Nigeria’s Maliyo Games develops mobile titles rooted in African cultural experiences, but most revenue still comes from advertising, commissions, or development partnerships rather than large-scale franchise licensing. This contrasts sharply with mature gaming markets, where successful titles generate significant income through spin-offs, merchandising, film adaptations, and branded collaborations.

Who Will Capture the Middleware Margin?

The structural bottlenecks in Africa’s gaming ecosystem point to a broader conclusion: the greatest financial upside may not lie with the developers themselves, but with the companies controlling the infrastructure between players and studios. So, three categories of intermediaries appear particularly well positioned.

Payment processors integrating mobile money could capture fees from millions of micro-transactions; while platform operators like global app stores already take significant shares through distribution and payment commissions. Regional publishers and aggregators may also play a growing role by helping studios scale across markets, manage localization, and connect with advertisers or investors.

For investors and industry observers, the key signal to watch is not simply gaming revenue growth. The real opportunity lies in the middleware infrastructure that connects African gamers to global digital markets. As the continent’s gaming audience continues to expand, the companies that solve Africa’s payment, distribution, and licensing bottlenecks may ultimately capture the largest share of the industry’s value.

{kind=link}