Table of Contents

In Summary:

- Nigeria leads with ~45% growth driven by pro-market central bank reforms, while Egypt (~38%) and Kenya (~30%) follow, powered by an IMF-backed recovery and strong domestic investors.

- Exchanges in Ghana (~22%), Tanzania (~20%), and Botswana (~16%) are rebounding strongly, primarily fueled by high global prices for gold and diamonds, coupled with debt management.

- Rwanda (~18%), Ivory Coast (~15%), and Mauritius (~12%) demonstrate that strategic governance, and regional integration are key catalysts for attracting investment and achieving steady market growth.

Deep Dive!!

Monday, 15 December, 2025 – In 2025, the narrative of African capital markets has decisively shifted from one of emerging potential to one of demonstrated, dynamic growth. Across the continent, a confluence of bold policy reforms, strategic economic diversification, and resurgent investor confidence is fueling a historic rally in stock market valuations. This article presents a definitive ranking of the ten African exchanges projected to achieve the highest market capitalization growth this year, offering a granular analysis of the unique drivers, that are rewriting the rules of investment on the continent.

This ranking is more than a snapshot of financial performance; it is a revealing map of divergent economic strategies and their tangible outcomes. We will explore how traditional resource powerhouses are leveraging commodity booms to finance deeper market development, while service-driven economies are capitalizing on digital disruption and regional integration. Through verified data, central bank reports, and direct insights from market leaders, the following analysis uncovers the compelling stories behind the percentages, illustrating how Africa's most progressive economies are harnessing their capital markets not merely as trading venues, but as powerful engines for sustainable development and wealth creation.

10. Mauritius

The Stock Exchange of Mauritius (SEM) is projected to achieve a robust 12% growth in market capitalization in 2025, a figure that underscores its resilience as a stable international financial gateway rather than a high-growth frontier market. This growth is primarily anchored by the sustained, high-value recovery of its cornerstone hospitality and tourism sector.

Major listed groups like New Mauritius Hotels and Sun Resorts have reported that occupancy and average daily rates for premium properties have not only returned to but in some segments exceeded 2019 levels, driven by a strategic focus on high-spending European and Middle Eastern tourists. A senior analyst from Mauritius Commercial Bank (MCB) Group noted, "The luxury segment's rebound has significantly boosted revenues and profitability for listed entities, providing a solid earnings foundation for market valuations."

Concurrently, the exchange's strategic positioning as a gateway for investment into Africa continues to attract capital flows, with its Global Business Sector facilitating numerous funds and holding companies listed on the SEM that invest across the continent. The stability offered by its AA- rated sovereign credit profile and well-regulated exchange provides a unique safe-haven appeal, attracting conservative capital seeking diversified exposure to African growth while mitigating direct operational risks prevalent in larger continental economies.

9. Ivory Coast

As the undisputed economic engine of the West African Economic and Monetary Union (WAEMU), Ivory Coast leverages the regional Bourse Régionale des Valeurs Mobilières (BRVM) to drive an estimated 15% market cap growth. The growth is fundamentally powered by the country’s consistent real GDP expansion, which the IMF projects at 6.5% for 2025, creating a powerful tailwind for corporate earnings.

Major listed agri-industrial champions, such as SIFCA (palm oil, rubber) and Olam-owned entities in cocoa processing, benefit from a dual advantage: sustained high global commodity prices and a national policy push for increased local value-addition, which improves their profit margins. The banking sector, led by giants like Société Générale de Banques en Côte d'Ivoire (SGBCI), thrives on financing this broad-based economic activity, with loan books expanding in tandem with GDP.

The BRVM's unique structure as a single, integrated regional exchange for eight Francophone nations is a critical multiplier. It provides Ivorian-listed companies, which constitute over 70% of the exchange's total capitalization with access to a deeper, regionally diversified investor pool, enhancing liquidity and valuation stability. As noted in a recent BRVM market report, "The integration allows performance shocks in one member state to be absorbed by capital from others, creating a more resilient valuation platform for Ivorian assets."

8. Botswana

The Botswana Stock Exchange (BSE) anticipates a 16% capitalization increase, a direct testament to its model of disciplined macroeconomic management and prudent fiscal stewardship. The primary catalyst is the stabilization and recovery of the global diamond market, following a period of inventory correction in 2023-24.

As the world's leading producer of gem-quality diamonds by value, Botswana's state revenues from Debswana (a 50/50 joint venture with De Beers) have rebounded sharply. This replenishment of fiscal coffers improves sovereign credit metrics and overall economic sentiment, indirectly boosting confidence in listed corporates. Domestically, the formidable and growing investment power of local pension funds and asset managers is the bedrock of market liquidity.

The Botswana Public Officers Pension Fund (BPOPF) and others maintain significant, strategic allocations to domestic equities, providing a non-speculative, long-term bid for blue-chip stocks in banking, like First National Bank Botswana (FNBB), and retail. As articulated by the CEO of a leading asset manager in Gaborone, "Our pension regulations and the sheer size of local savings create a natural, stable buyer base for quality listings, insulating our market from the extreme volatility seen in other frontier exchanges." This model prioritizes organic, savings-driven development over volatile foreign "hot money" flows.

7. Rwanda

The Rwanda Stock Exchange (RSE) is set for impressive growth of approximately 18%, showcasing a paradigm of how strategic governance and innovation can accelerate capital market development in a small, landlocked nation. Rwanda’s globally recognized reputation for strong institutional governance, efficiency, and low corruption significantly reduces the country risk premium demanded by international investors.

This was highlighted in a 2024 World Bank Ease of Doing Business assessment, which consistently ranks Rwanda among the top reformers in Africa, making its equity assets comparatively more attractive. A transformative driver is the rapid development of the Kigali International Financial Centre (KIFC), which has enacted a modern commercial law framework based on English common law to attract cross-listings and facilitate new capital-raising.

While the market remains compact, dominated by Bank of Kigali and Bralirwa, the government's focused policy is broadening its appeal. "The KIFC is not just about creating another exchange; it's about building a full ecosystem, from fund administration to arbitration, that makes Rwanda a plausible hub for channeling investment into the heart of Africa," explained the KIFC's Chief Executive. This ecosystem-building approach is slowly attracting attention from regional companies considering secondary listings.

6. Tanzania

The Dar es Salaam Stock Exchange (DSE) is expected to see a 20% rise in market capitalization, fueled by a powerful synergy between strategic commodity wealth and transformative public investment. A historic surge in global gold prices, breaching the $2,400 per ounce mark in 2025, has directly supercharged the profitability and market valuation of major listed producers like AngloGold Ashanti's Geita Mine. This has generated substantial foreign earnings, strengthened the national balance of payments, and improved fiscal health, as reported in the Bank of Tanzania's monthly economic reviews.

The government is strategically channeling this commodity-driven windfall into ambitious public infrastructure spending, including the Standard Gauge Railway and Julius Nyerere Hydropower Project, which in turn stimulates the industrial and manufacturing sectors. Listed conglomerates such as Tanzania Portland Cement and Twiga Cement are direct beneficiaries of this construction boom.

The sustained political stability and policy predictability under the current administration have encouraged a notable increase in participation from East African regional investors, who view Tanzania as a stable, resource-rich play. A fund manager from Kenya's Genghis Capital noted, "Tanzania offers a compelling mix of resource exposure and infrastructure-led growth, all within a increasingly predictable political environment."

5. Ghana

Following a challenging sovereign debt restructuring, the Ghana Stock Exchange (GSE) is rebounding with a projected 22% growth, signaling one of the continent's most dramatic returns of investor confidence. The successful completion of the domestic debt exchange program (DDEP) in late 2024 was a painful but necessary catharsis. It removed a massive systemic overhang from the banking sector's balance sheets, allowing for a sharp repricing of risk.

Banking stocks, which were heavily discounted, have led the market recovery as their capital adequacy positions stabilize and net interest margins remain wide amidst a high-rate environment. Externally, the sustained high price of gold, Ghana's top export, has been a lifesaver, accelerating foreign reserve accumulation at the Bank of Ghana and contributing to a period of relative currency stability. This improved macroeconomic backdrop benefits all listed firms.

"The gold sector's performance and the resolution of the debt crisis have been the twin pillars of our market's recovery. Investors are now looking past the restructuring and seeing fundamentally undervalued assets," stated the Managing Director of the GSE. This recovery exemplifies a market leveraging its inherent resource strengths to finance a broader economic rehabilitation.

4. South Africa

Africa's most mature and liquid exchange, the Johannesburg Stock Exchange (JSE), is forecast to grow by 25%, a performance driven by its irreplaceable dual role as a deep-value resource play and a sophisticated financial hub.

The Financials and Technology sector, overwhelmingly dominated by the global heavyweight Naspers/Prosus, remains a critical conduit for international capital. Its performance is tightly correlated with global tech sentiment, providing a form of portfolio diversification for foreign investors allocating to Africa. Simultaneously, the traditional Mining sector experiences a strong upcycle, driven by cyclical demand for platinum group metals (PGMs) in automotive and industrial applications, as well as sustained high gold prices. A weaker South African Rand throughout much of 2025 has further amplified the Rand-denominated profits of these export-heavy companies. Despite persistent domestic challenges, notably the ongoing energy crisis managed through "loadshedding," the JSE's unparalleled depth, robust regulatory framework (based on a twin-peaks model), and diverse listings, from global breweries to telecommunications giants, cement its status.

As a portfolio manager from Ninety One remarked, "For large-scale institutional allocation to Africa, the JSE's liquidity and regulatory sophistication are non-negotiable. It is the continent's undeniable primary market."

3. Kenya

The Nairobi Securities Exchange (NSE) demonstrates resilient growth of 30%, underpinned by a unique blend of deep domestic institutional strength and homegrown technological disruption. The market's bedrock is a deep pool of local institutional investors, with pension funds and SACCOs (Savings and Credit Co-Operatives) controlling assets under management exceeding $15 billion.

Their consistent, long-term demand for blue-chip equities, particularly in the dominant banking sector (Equity Group, KCB Group), provides a formidable stabilising floor for market valuations that many frontier markets lack. The outsized influence of Safaricom, which alone often constitutes over 40% of the NSE's capitalization, continues to anchor the entire index.

Its forays into expansive new digital ecosystems, particularly M-Pesa's evolution into a full-scale financial services platform, drive its growth narrative and, by extension, that of the entire market. Furthermore, Kenya's vibrant tech startup ecosystem, dubbed "Silicon Savannah," generates immense positive spillover effects. While most startups are not yet on the main board, their success, evinced by significant venture capital inflows, enhances the country's profile as a dynamic, innovative investment destination, attracting interest in listed tech-adjacent firms. "The NSE is a tale of two strengths: the unwavering support of local pensions and the transformative national champion that is Safaricom. Together, they create a resilient core," observed an analyst from Sterling Capital.

2. Egypt

The Egyptian Exchange (EGX) is staging a dramatic, liquidity-driven recovery with an estimated 38% surge, directly tied to a fundamental and long-awaited macroeconomic policy reset. The cornerstone is the $8 billion Extended Fund Facility with the IMF secured in late 2024, which unlocked an additional $14 billion in multilateral and bilateral funding. This program mandated critical reforms, restoring a crucial degree of faith among international institutional investors who had largely exited the market.

The most pivotal policy shift was the central bank's commitment to a permanently flexible exchange rate, finally eliminating a chronic foreign currency shortage that had crippled the economy for years. The subsequent large devaluation and unification of the exchange rate immediately made Egyptian equities appear deeply undervalued to foreign capital, triggering a powerful wave of re-rating. This is supercharged by an aggressive government privatization program ("The State Ownership Policy"), which aims to offer strategic stakes in dozens of major state-owned enterprises across banking, energy, and industry.

The successful IPO of shares in leading banks has already injected billions in new market capitalization. A senior director at EFG Hermes, Egypt's leading investment bank, stated, "The float of the pound was the necessary shock. Combined with the IPO pipeline, it has fundamentally changed the liquidity and investability thesis for Egypt almost overnight."

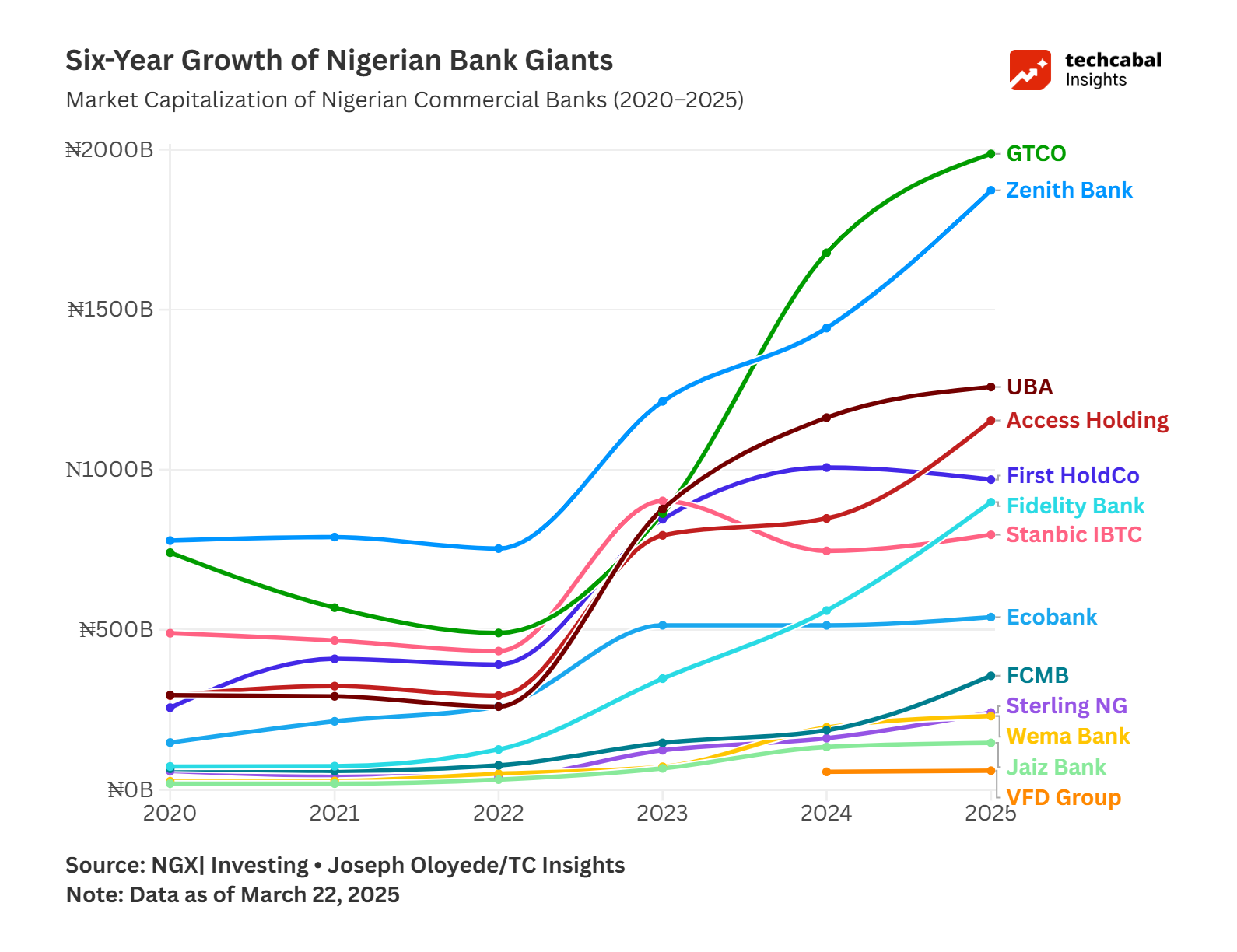

1. Nigeria

The Nigerian Exchange (NGX) is poised to be Africa's unequivocal top performer in 2025, with market capitalization expected to soar by approximately 45%, marking a historic comeback. This phenomenal growth is the direct reward for a series of bold, market-friendly monetary policy reforms initiated by the Central Bank of Nigeria (CBN) under its new leadership from mid-2024.

The clearance of the longstanding FX backlog, the move towards a single, market-reflective exchange rate in the Nigerian Autonomous Foreign Exchange Market (NAFEM), and the lifting of arbitrary trading restrictions triggered an unprecedented return of foreign portfolio investment. After years of net outflows, FPIs turned decisively positive, with inflows in Q1 2025 alone reportedly exceeding the total for the preceding three years. This macro stability has directly translated into record-breaking corporate earnings, particularly in the banking sector.

Tier-1 lenders like Access Holdings and UBA reported staggering year-on-year profit growth exceeding 300% for the first half of 2025, fueled by high interest margins, currency revaluation gains, and robust trading income. The growth narrative is further amplified by landmark listings from the government's reform agenda, most notably the highly anticipated IPO of NNPC's retail subsidiary. As the NGX CEO, Temi Popoola, proclaimed, "We are witnessing a fundamental rewiring of the Nigerian economy. Capital that was trapped in opaque systems is now being channeled into transparent, publicly-traded vehicles, deepening our market at an exponential rate." This symbolizes a profound shift of national wealth onto the exchange, solidifying its role as the continent's premier growth story for the year.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].

{kind=link}