Table of Contents

IN JULY of last year, in offices in Nairobi and London, lawyers from Clifford Chance closed a deal that few outside the off-grid solar industry noticed. Sun King, a seller of small solar systems to East African households, raised $156m in Kenyan shillings (equivalent), backed by the future repayments of roughly 1.4m of its Kenyan customers. Five Kenyan commercial banks—Absa, Co-operative, KCB, Stanbic and Citi's local arm—took the senior tranche (lowest risk portion of debt issue that is paid first). Three development banks took the mezzanine (higher risk portion of debt issue, paid after the senior tranche). It was the largest securitisation completed anywhere in sub-Saharan Africa outside South Africa.

That is a curious sentence to write about a business built on $0.19 daily payments. But the deal, and others like it, point to a structural shift in how African energy access gets financed.

How PAYG solar players are securitising Kenyan receivables

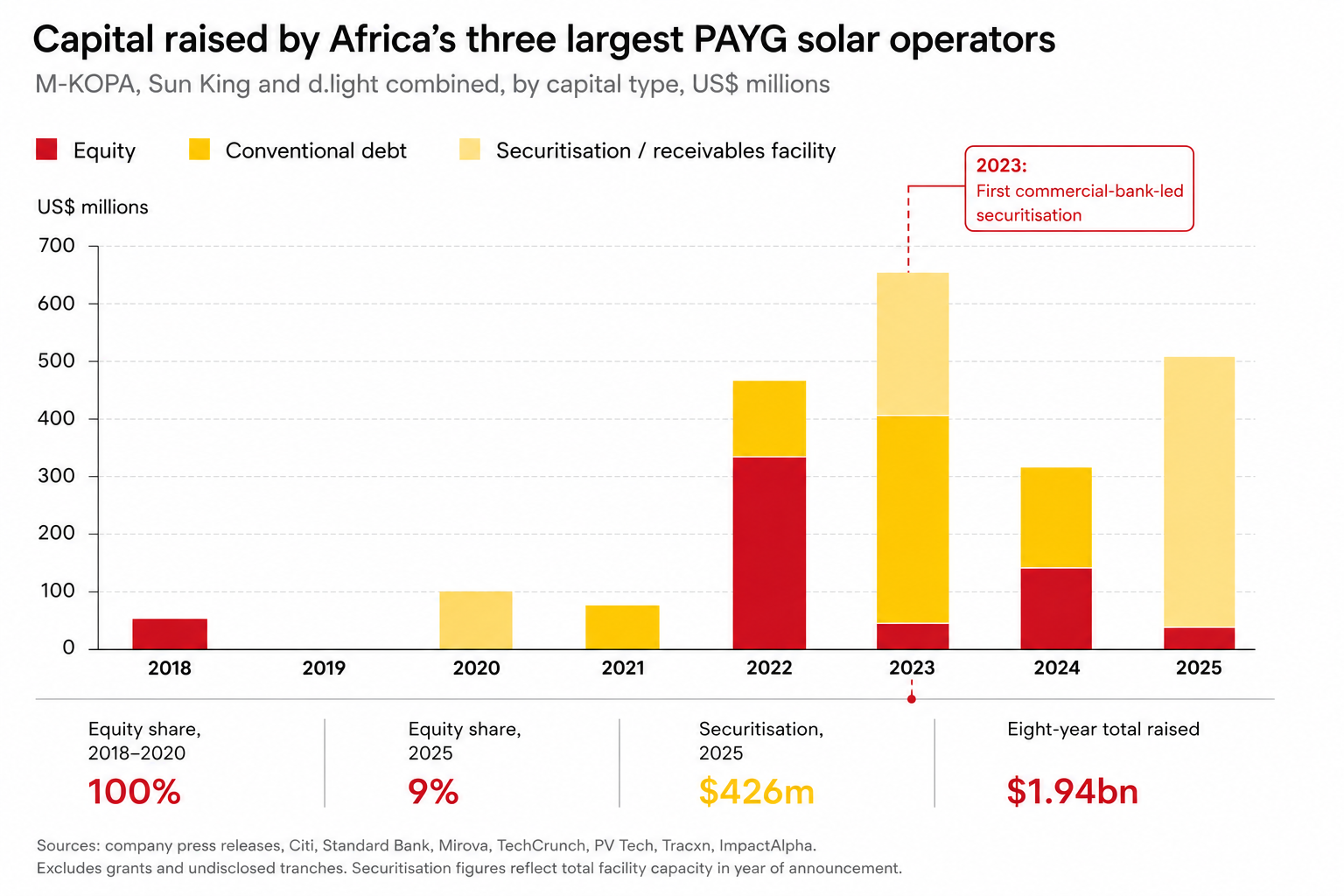

For most of its history, pay-as-you-go (PAYG) solar in Africa ran on equity. Companies such as M-KOPA, Sun King, d.light and Bboxx sold solar home systems on credit to households earning a few dollars a day. The receivables that resulted—millions of tiny mobile-money payments in volatile local currencies—were too small, too opaque and too unfamiliar for international lenders to underwrite. Growth was funded by venture capitalists and concessional grants.

This funding structure has started to change, starting in Kenya. In May 2023 Sun King and Citi closed the first bank-led, shilling-denominated securitisation in the sector: $130m, structured around the firm's existing and future customer payments. Eight months later d.light, an American firm with deep Kenyan operations, announced that its $110m Brighter Life Kenya 1 facility had repaid its senior debt in full and ahead of schedule, entirely from operating cash flow. It was the first time the off-grid solar industry had demonstrated that its receivables actually produced cash.

Other deals followed. M-KOPA, the largest of the operators by customer count, secured over $200m in sustainability-linked debt led by Standard Bank, Africa's biggest lender. The International Finance Corporation, FMO of the Netherlands, and British International Investment all took pieces. Sun King's second Kenyan securitisation, the $156m deal last July, doubled down on the model. Across Kenya alone, the firm has now extended $1.3bn in solar loans to nearly 10m customers continent-wide; in Kenya specifically, an estimated three in ten households have access to its products.

Three things made Kenya work. M-Pesa, the mobile-money system, gave operators a payments rail and a customer-level data trail. The country's commercial banks—particularly Stanbic and KCB—were willing to underwrite the resulting paper on their own balance sheets, not merely as agents for foreign lenders. And the Capital Markets Authority allowed private offers that did not require the full machinery of a public bond issue. None of those conditions is universal across Africa.

Why Nigeria is harder

Nigeria ought to be the bigger market. It has more than 200m people, an electricity grid that produced just 3,940 megawatts at one March 2026 reading, and one of the largest off-grid solar markets on the continent. The country imported some 2.9m solar panels worth ₦435bn in 2025 alone, according to its foreign trade statistics. M-KOPA reports that Nigeria is its fastest-growing market, with ₦231bn ($150m at current rates) in cumulative credit extended.

Yet no operator has closed a Nigerian-naira-denominated securitisation that resembles the Kenyan deals. The reasons are instructive.

Begin with the currency. The naira has lost more than two-thirds of its dollar value since mid-2023, when the central bank began unwinding its multiple exchange-rate regime. For a securitisation, that creates a problem of asset-liability matching: the receivables are in naira, but the equity cushions, the credit enhancements, and often the operators' own corporate liabilities are in dollars. Hedging is expensive where it exists at all. Sun King has raised local-currency capital in Nigeria and Tanzania alongside Kenya—some $450m cumulatively—but its headline securitisations remain shilling-denominated and concentrated in Kenya, underscoring how difficult these structures are to replicate in more volatile currency markets like Nigeria.

Banking depth is the second issue. Kenya's top commercial banks have the appetite and the balance sheets to take meaningful tickets on receivables paper. Nigerian banks, weighed down by exposure to a power sector that owed generators ₦6.8trn as of February 2026 and by their own capital-raising requirements, have less room. Foreign banks remain wary.

The third constraint is regulatory. Kenya and Côte d'Ivoire are the only African jurisdictions piloting social asset-backed securities (ABS) frameworks with any depth. Nigeria's Securities and Exchange Commission has rules permitting securitisation, but no PAYG operator has yet tested them. The lack of standardised, audited repayment data across the industry—a problem the off-grid sector has not fully solved—compounds the regulatory caution. In some ways, the off-grid sector now faces a challenge similar to the one mobile-money lenders solved a decade ago: converting fragmented behavioral repayment data into a standardized financial asset. Companies like JUMO built the infrastructure layer for digital credit. PAYG solar may require a comparable layer for securitised energy receivables.

There are reasons for optimism. The federal government's Distributed Access through Renewable Energy Scale-up (DARES) programme, backed by a $750m World Bank loan, helped drive a 33% year-on-year increase in Nigerian PAYG solar sales in the first half of 2025. The DARES money crowds in private capital rather than crowding it out, by reducing the unit economics risk for operators. And M-KOPA's Nigerian loan book, however funded, demonstrates that the receivables exist. The question is when, and through which operator, the first naira-denominated PAYG securitisation closes. It is a matter of timing rather than possibility.

Why capital has become the moat in PAYG solar

Step back from the country detail and a broader shift comes into view. The off-grid solar industry's centre of gravity is moving from equity to debt, and that move has consequences.

It changes who can compete. Securitisation requires audited collections data, standardised key performance indicators, and a multi-year track record of customer repayment. Companies that have built that discipline—Sun King, d.light, M-KOPA—can now fund customer growth at debt prices rather than diluting their equity at venture valuations. Companies that have not are at a structural disadvantage that did not exist five years ago. The four largest operators are pulling away from a long tail.

It changes the role of development finance. Institutions such as the IFC, BII, FMO and Norfund used to be the senior lenders to this sector. They are now migrating into mezzanine tranches and credit enhancement, leaving the senior debt to commercial banks. That is the textbook function of development finance—to de-risk private capital rather than substitute for it—and it is finally happening at scale.

It does not, however, mean the market is finished. As Ecofin Agency noted last September, M-KOPA's $1.5bn in cumulative receivables "could be securitised but lack scale, trust and regulatory clarity". Most PAYG operators still rely on internal repayment metrics not independently audited to international standards. African pension funds, the natural buyers of long-dated local-currency paper, are largely absent from these structures. The maturation is real but partial.

What might come next in the financing of PAYG solar companies?

Three things will determine whether the next 18 months extend the Kenyan template or expose its limits. The first is whether Sun King, M-KOPA or d.light attempts a Nigerian-naira-denominated securitisation. A first deal would matter less for its size than for the precedent it sets. The second is whether African pension funds begin to participate. The continent's largest pools of long-dated local-currency savings remain almost entirely uninvested in the sector that most resembles their liability profile. The third is whether the DARES programme in Nigeria and the ASCENT programme regionally accelerate private capital or distort it; subsidy regimes have a habit of changing the unit economics of the businesses they support, sometimes for the worse.

For investors and operators, the practical message is straightforward. The PAYG solar industry has crossed a threshold. The companies that can issue debt now have an advantage that compounds. The markets that can host that debt locally—Kenya today, perhaps Nigeria tomorrow—will attract the capital. The rest will wait.