Table of Contents

In Summary

• Africa’s public debt has risen sharply over the past decade as governments borrowed to fund infrastructure, social programmes, and economic stabilization. By 2026, several countries are expected to have debt levels equal to or higher than their total annual economic output.

• High debt across the continent is being driven by weak tax systems, unstable currencies, commodity price swings, repeated global shocks, governance challenges, and costly borrowing.

• While a few countries have made progress through debt restructuring and IMF or World Bank support, many still face heavy debt-servicing and refinancing pressures as growth and exports remain weak.

• Rising debt is limiting governments’ ability to spend on health, education, and development, increasing the risk of prolonged fiscal and economic strain across the region.

Deep Dive!!!

Africa’s debt crisis is often described as a single continental problem, but in reality it is a collection of very different national stories. By 2026, some governments have managed to stabilize their debt through reforms and restructuring, while others have slid deeper into financial distress, with debt now larger than the size of their entire economies.

Debt-to-GDP ratios matter because they show how much room a government has to function. When debt is low, countries can invest in schools, hospitals, and infrastructure. When debt is high, a growing share of public money is diverted toward interest payments, leaving less for development and making governments more vulnerable to economic shocks.

The countries that appear at the top of Africa’s 2026 debt rankings share several underlying weaknesses. Many depend heavily on a narrow range of exports, such as oil, copper, or tourism. Others have weak tax systems that limit their ability to raise revenue at home. When global prices fall, currencies weaken, or external financing dries up, these economies are forced to borrow more just to keep basic services running.

In several cases, debt was accumulated in good faith to fund growth like building roads, ports, power plants, and social programmes. But delays in returns, cost overruns, corruption, and political instability meant that these projects did not generate enough revenue to cover the loans used to build them. Over time, temporary borrowing turned into permanent debt.

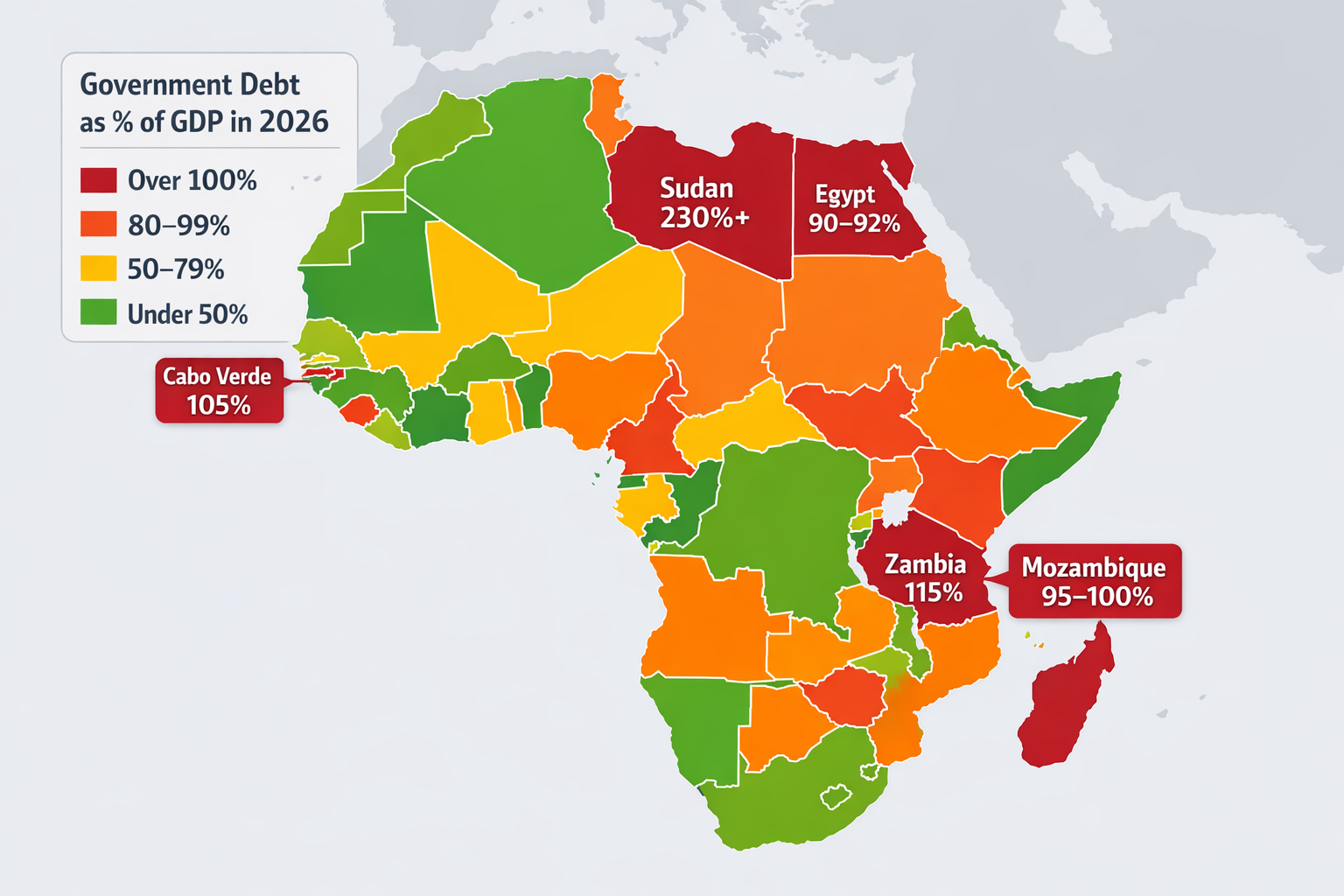

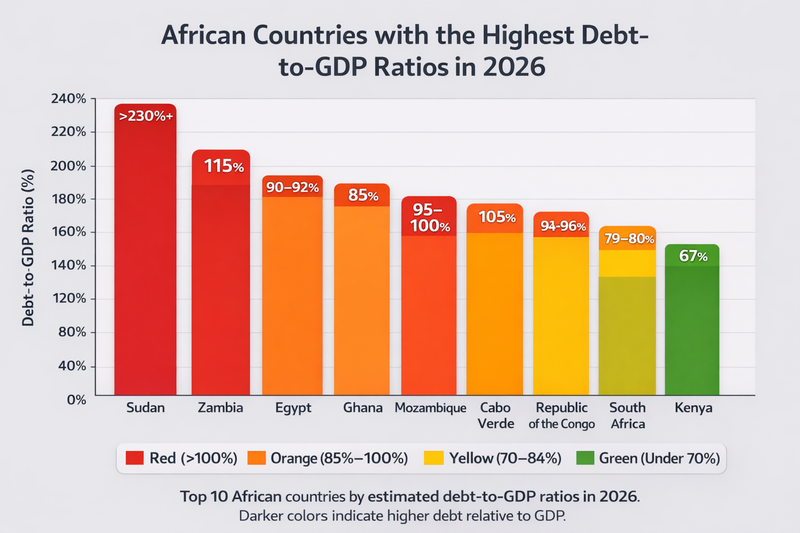

Africa: Estimated Debt-to-GDP Ratios in 2026

10.Kenya

Kenya enters 2026 as one of Sub-Saharan Africa’s fastest-growing large economies, yet its public debt position continues to constrain fiscal flexibility. Real GDP expanded by 4.9 percent in the first quarter of 2025, with full-year growth projected at about 4.8 percent, above the regional average of 3.7 percent. Growth has been driven by services, construction, and a gradual recovery in domestic demand, reinforcing Kenya’s role as an economic anchor in East Africa even as fiscal pressures persist.

According to the Central Bank of Kenya, total public debt reached Kshs 11.5 trillion as of May 2025, up from Kshs 10.4 trillion a year earlier. This increase reflects continued budget deficits and refinancing needs rather than new large-scale expansionary projects. Based on National Treasury GDP estimates, Kenya’s debt-to-GDP ratio stood at approximately 67.4 percent at the end of 2024, down from 73.4 percent in 2023 following currency appreciation and stronger nominal growth. While the ratio has improved, it remains well above the IMF’s indicative 50 percent threshold for developing economies, placing Kenya in the high-risk debt distress category.

Debt composition has shifted decisively toward domestic borrowing. External public debt stood at Kshs 5.3 trillion in May 2025, rising marginally from Kshs 5.1 trillion in May 2024, partly due to active liability management. The February 2025 partial buyback of the USD 900 million Eurobond, financed through a new USD 1.5 billion issuance, helped smooth near-term maturities and stabilize investor sentiment. Domestic debt, however, rose sharply to Kshs 6.2 trillion from Kshs 5.3 trillion over the same period, driven by constrained access to external financing and easing domestic interest rates. By May 2025, domestic debt accounted for 53.9 percent of total public debt, reversing the external-heavy structure seen during the currency depreciation of 2023.

Despite improved refinancing outcomes, debt servicing costs remain elevated and continue to absorb a growing share of government revenues. Kenya’s sovereign credit ratings remain in speculative territory, reflecting high credit risk but continued capacity to meet obligations. However, sentiment has begun to stabilize. In January 2025, Moody’s affirmed Kenya’s Caa1 rating and revised the outlook from negative to positive, citing improved revenue collection, prudent debt management, and reduced short-term external refinancing pressure.

Fiscal consolidation efforts are evident in the FY 2025/26 budget, which projects revenue growth to Kshs 3.4 trillion, equivalent to 17.5 percent of GDP, against projected expenditure of Kshs 4.3 trillion, or 22.3 percent of GDP. The resulting fiscal deficit is expected to narrow to 4.8 percent of GDP. However, execution risks remain high. Business conditions weakened in mid-2025, with the Purchasing Managers’ Index slipping into contraction territory amid political unrest, high living costs, and elevated fuel prices, all of which threaten revenue performance.

Kenya’s debt challenge is structural rather than episodic. Over the past decade, persistent fiscal deficits and faster expenditure growth have driven total public debt from Kshs 3.4 trillion in 2016 to Kshs 11.5 trillion in 2025. While economic growth provides a buffer against crisis, Kenya’s experience underscores a broader continental reality in 2026: growth alone is insufficient to resolve debt pressures unless revenue mobilisation, expenditure discipline, and export performance consistently outpace borrowing.

9. South Africa

South Africa, Africa’s most industrialized economy, carries a large public debt stock relative to GDP that reflects decades of fiscal deficits and support for state-owned enterprises. According to IMF-aligned estimates, the country’s debt-to-GDP ratio is projected at approximately 79–80% in 2026, up from lower levels earlier in the decade.

Unlike many peers, a substantial share of South Africa’s debt is domestic, which limits foreign exchange risk but intensifies refinancing pressures in local markets. Debt servicing continues to compete with priority social and infrastructure spending, and rating agencies have flagged South Africa’s high debt load as a constraint on public investment.

South Africa also holds a large share of Africa’s external debt; a 2025 Afreximbank report noted that South Africa alone accounts for around 13.1% of the continent’s external debt stock, highlighting its outsized role in regional financial dynamics.

8. Mozambique

Mozambique enters 2026 with a debt-to-GDP ratio projected between 95 and 100 percent, reflecting a prolonged combination of historical borrowing, previously undisclosed loans, and large infrastructure investments. Following revelations in 2013 of government-backed loans linked to maritime security and tuna fishing projects, international financing was disrupted, eroding investor confidence and limiting access to affordable credit. Although the country has received multilateral support and undertaken fiscal adjustments, debt pressures remain elevated.

Infrastructure investments, especially in transport and energy, have relied on a mixture of external and domestic financing. Delays in expected revenue from offshore natural gas projects have compounded fiscal pressures, making near-term debt servicing a significant constraint on government expenditure. IMF reports indicate that debt service absorbs a substantial share of revenues, limiting spending on health, education, and social programs.

Exchange rate volatility further amplifies Mozambique’s debt burden, as a large portion of obligations are external and denominated in foreign currency. Despite gradual economic recovery, fiscal space remains tight, and structural vulnerabilities persist. Mozambique’s case highlights how ambitious development projects, even in resource-rich contexts, can elevate sovereign leverage when financing outpaces revenue realization.

7. Republic of the Congo

Estimated debt-to-GDP ratio (2026): approximately 94–96 %

The Republic of the Congo’s public debt has been among the most volatile in Central Africa, shaped by heavy reliance on oil receipts, fluctuating commodity prices, and evolving debt composition that increasingly leans on domestic financing. According to World Bank data, Congo’s total public debt fell to 93.5 % of GDP in 2024, down from highs above 100 % in prior years, as rising crude prices allowed the government to service more external obligations and reduce foreign liabilities.

The shift in debt composition has been significant. According to an IMF Country Report, external debt accounted for approximately 34.7 % of GDP by end-2024, a decline from over 43 % in 2022, driven by repayments on oil-linked commercial obligations and favorable pricing terms. Simultaneously, domestic debt increased sharply, rising to nearly 59 % of GDP by late 2024 as the government issued Treasury securities to finance budget gaps and consolidate arrears.

Economic dynamics are critical for understanding Congo’s debt pressures. Growth in 2024 remained modest at around 2.6 % as oil revenue trends stabilized and revenue mobilisation concentrated heavily in the extractive sector. The substantial share of domestic public securities outstanding in the Central African Economic and Monetary Community (CEMAC) market amplifies refinancing needs, as regional investors demand higher yields amid liquidity constraints.

Debt servicing has absorbed a large portion of fiscal resources; by late 2024, debt service accounted for about half of tax revenues, forcing expenditure restraint in other areas such as social services and infrastructure. Liquidity pressures have also led to arrears, which the authorities have sought to address through debt reprofiling strategies that extended maturities and reduced near-term cash flow strain.

Looking ahead, Congo’s debt ratio is projected to remain elevated near the mid-90s as a share of GDP in 2026, with refinancing risk and liquidity management posing continuing challenges. The reliance on oil, still an estimated 70–80 % of export revenue means that global energy price shifts heavily influence fiscal space, and domestic securities pressures could crowd out private credit if not carefully managed.

6. Cabo Verde

Estimated debt-to-GDP ratio (2026): approximately 105–108 %

Cabo Verde stands out among high-debt African states not for large absolute borrowing but because its relatively small economic base cannot absorb moderate debt without pushing the ratio above critical thresholds. According to recent IMF staff estimates, Cabo Verde’s public debt was expected to be around 104.9 % of GDP by end-2025, and while continued fiscal consolidation is projected to modestly lower the ratio by 2026, the level remains above 100 % one of the highest in West Africa.

The IMF’s Debt Sustainability Analysis (DSA) completed in early 2025 judged Cabo Verde to be at high overall risk of debt distress and moderate risk of external debt distress, even as near-term servicing needs were assessed as manageable. This nuanced classification reflects a debt stock that is large relative to economic output but carried at favorable terms, with a mix of concessional external loans and domestic obligations that have muted short-term rollover pressures.

Cabo Verde’s fiscal picture is shaped by a rebound in tourism, the economy’s dominant sector and a strong macroeconomic performance that saw inflation fall sharply to around 1 % in 2024, helping ease cost-of-living pressures and support real GDP growth. The World Bank’s 2025 Economic Update reported that tourism-led growth and prudent fiscal management contributed to central government debt of around 110.2% of GDP, while a current accounting surplus for the first time in years pointed to improving external balances.

Despite these positives, structural constraints make Cabo Verde especially vulnerable. The economy is heavily dependent on external goods and services, with import reliance and climate-related risks amplifying exposure to global shocks. Fiscal targets embedded in IMF programmes and supported by extended credit facilities (ECF and RSF arrangements) emphasize strengthening revenue mobilisation, controlling contingent liabilities from state enterprises, and improving public investment efficiency to support long-term debt reduction efforts.

In practical terms, little slack remains in Cabo Verde’s budget. Public investment commitments, climate adaptation spending, and social programmes must be balanced against ongoing debt service, requiring careful prioritization and structural reform if the country is to reach medium-term debt targets below 70 % of GDP by the early 2030s.

5. Ghana

Estimated debt-to-GDP ratio in 2026: about 85 percent

Ghana’s debt profile in 2026 reflects the aftermath of one of the most significant sovereign debt crises in Sub-Saharan Africa in recent years. After debt levels surged above sustainable thresholds in the early 2020s, Ghana entered a comprehensive restructuring process supported by the IMF, bilateral creditors, and private bondholders.

IMF projections indicate that Ghana’s debt-to-GDP ratio is expected to decline to around 85 percent by 2026, down from the peak levels recorded before restructuring. This improvement reflects debt exchanges, maturity extensions, and fiscal consolidation measures aimed at restoring macroeconomic stability.

Despite progress, Ghana’s debt burden remains high. Interest payments continue to absorb a substantial share of government revenues, while exchange rate volatility increases the cost of servicing external obligations. The country’s experience highlights both the effectiveness and the limits of restructuring. While immediate liquidity pressures have eased, long-term sustainability depends on stronger revenue mobilization, export growth, and disciplined fiscal management.

4. Tunisia

Estimated debt‑to‑GDP ratio in 2026: about 80–82 percent

Tunisia’s public finances have faced sustained pressures over much of the past decade, and by 2026 the country continues to carry a high level of sovereign debt relative to the size of its economy. According to aggregated macroeconomic projections from global macro models and official data, Tunisia’s government debt reached nearly 80 percent of GDP in 2024, and is expected to trend slightly higher toward 82 percent in 2026 without strong structural adjustments.

Persistent budget deficits have been a defining feature of Tunisia’s fiscal landscape, driven by high public expenditure on subsidies, public wages, and social programmes amid only modest revenue growth. A 2025 report indicated that public debt was expected to peak at approximately TND 147.5 billion (about USD 50 billion) by the end of 2025, equivalent to roughly 81 percent of GDP, with domestic debt accounting for around 57 percent of the total and foreign obligations comprising the remainder.

Economic growth has been constrained by political uncertainty, weakening investment, and slow tourism recovery, which together have limited export expansion and tax revenues. Continued reliance on external financing combined with domestic borrowing has increased medium‑term debt servicing costs and contributed to a widening budget gap. In late 2025, Reuters reported that Tunisia planned to seek direct financing of USD 3.7 billion from its central bank to fill a growing fiscal deficit in 2026, highlighting ongoing pressures on the government’s financing strategy.

Tunisia’s debt profile illustrates the challenge of balancing short‑term budget needs against long‑term sustainability. While the country has avoided the highest debt brackets seen elsewhere in Africa, its debt dynamics remain fragile, with significant exposure to changes in interest rates, exchange rate movements, and investor sentiment. Strengthened revenue mobilisation, tighter expenditure control, and structural reforms aimed at stimulating private sector growth will be critical to ensure the debt burden does not escalate further relative to economic output.

3.Egypt

Estimated debt-to-GDP ratio in 2026: about 90 to 92 percent

Egypt remains one of Africa’s largest and most systemically important borrowers. IMF country reports place Egypt’s public debt below the extreme levels seen in some peers, but still high by international standards. Debt ratios stood just under 90 percent of GDP in 2025, with projections pointing to a slight increase toward the low 90s in 2026.

Persistent fiscal deficits, rapid population growth, and large-scale public investment projects have driven borrowing over the past decade. At the same time, currency adjustments and rising interest rates have increased the local currency cost of external debt servicing. Egypt’s debt structure includes a significant share of domestic borrowing, which reduces currency risk but raises refinancing and interest cost pressures.

Continued engagement with the IMF has helped stabilise foreign reserves and anchor reform efforts, but debt servicing remains a major constraint on fiscal flexibility. Egypt’s case illustrates how even diversified, large economies can face sustained debt pressure when growth and revenues struggle to keep pace with financing needs.

2. Zambia

Estimated debt-to-GDP ratio in 2026: about 115 percent

Zambia’s debt trajectory remains one of the most closely watched on the continent. Following its 2020 default, the country underwent prolonged negotiations with official and private creditors under the G20 Common Framework. While restructuring agreements have reduced immediate repayment pressures, the overall debt stock remains high.

Reuters and IMF reporting indicate that Zambia’s debt-to-GDP ratio is expected to hover around 115 percent in 2026. This reflects a combination of legacy borrowing, slower-than-expected economic recovery, and currency depreciation that has inflated the local value of external obligations.

Zambia’s heavy reliance on copper exports continues to shape its fiscal outlook. When global copper prices weaken, government revenues fall quickly, increasing borrowing needs. Although restructuring has created fiscal breathing room, long-term sustainability will depend on export diversification and stronger domestic revenue mobilization.

Top 10 African countries by estimated debt-to-GDP ratios in 2026. Darker colors indicate higher debt relative to GDP, highlighting countries under extreme fiscal pressure

1. Sudan

Estimated debt-to-GDP ratio in 2026: above 230 percent

Sudan stands as Africa’s most indebted country by a wide margin. IMF and World Bank assessments consistently place Sudan’s public debt well above 200 percent of GDP, with estimates for 2026 ranging between 230 and 260 percent depending on assumptions about economic contraction and arrears accumulation.

Decades of conflict, sanctions, and economic isolation have devastated Sudan’s productive capacity. Public revenues are extremely limited, while large portions of external debt consist of arrears accumulated over many years. Periodic attempts at arrears clearance and debt relief have repeatedly been derailed by political instability and renewed violence.

Sudan’s extreme debt ratio reflects not only high nominal debt but also a severely compressed GDP base. Unlike other countries on this list, Sudan’s debt problem is fundamentally structural and political. Without sustained peace, institutional rebuilding, and comprehensive international support, traditional debt management tools offer little prospect of restoring sustainability.

Why it matters in 2026

Africa’s high debt-to-GDP ratios are not merely numbers; they signal tangible fiscal constraints and structural vulnerabilities. Many governments now face dual exposure: rising external debt servicing costs and growing domestic borrowing needs. Even countries with stabilizing headline debt levels are increasingly competing with private-sector credit markets, which can slow investment and economic diversification. Elevated debt service absorbs a significant portion of revenues, often crowding out spending on health, education, and infrastructure. In practical terms, citizens may experience slower public service delivery, higher borrowing costs for businesses, and increased vulnerability to global economic shocks.

What happens next?

Debt restructuring will remain central, with several countries relying on restructuring frameworks, bilateral negotiations, and domestic debt reprofiling. While this can stabilize short-term liquidity, it does not immediately reduce debt ratios without sustained economic growth.

IMF-supported programs continue to play an important role in restoring credibility, stabilizing currencies, and unlocking concessional financing. However, they cannot fully offset weak export performance or repeated external shocks.

Growth risks remain high, including slower global growth, commodity price volatility, and climate-related disruptions. Countries with high debt have limited buffers if growth underperforms projections.

Governments with elevated debt will face difficult choices between social spending, public investment, and debt repayments, with domestic borrowing increasingly competing with private-sector credit.

What the Rankings Mean for Africa in 2026

Africa’s highest debt-to-GDP ratios in 2026 reflect the cumulative effects of structural weaknesses, external shocks, delayed reforms, and constrained growth rather than borrowing alone. For many countries, debt financed reconstruction, social stability, and basic services rather than discretionary expansion.

The rankings highlight a widening divergence across the continent. While some economies stabilize or gradually deleverage, others remain locked in high-debt cycles where limited growth, currency pressures, and higher global interest rates reinforce fiscal stress. In 2026, Africa’s debt trajectory will be determined less by how much governments borrow and more by whether growth, exports, and institutions can finally outpace obligations.

{kind=link}