Table of Contents

In Summary

- Tayo Oviosu founded Paga to digitize cash and expand financial access across Nigeria, with a vision to reach Africa.

- Over 16 years, Paga has processed 460 million transactions worth ₦23 trillion (~US$44 billion).

- The platform serves 29 million users through an extensive agent network, creating thousands of direct and indirect jobs.

- Paga provides infrastructure to over 150 businesses, including SME tools like Doroki, supporting financial inclusion and enterprise growth.

- Its hybrid agent-plus-digital model remains a rare differentiator, enabling it to scale deeper and faster than most African fintechs.

Deep Dive!!

Lagos, Nigeria, Wednesday, November 26 - Across Africa, financial exclusion remains a persistent barrier. Nearly 60% of sub-Saharan Africans lacked access to formal financial services as of 2023, according to the World Bank.

Yet mobile-phone penetration continued to rise across the continent, creating a massive gap and an opportunity for digital payment solutions.

Tayo Oviosu saw an opportunity to change that. In 2009, he founded Paga, a digital payment platform designed to bring secure, accessible, and scalable financial services to millions of Nigerians and, ultimately, to Africa at large.

Beyond individual transactions, Paga provides critical infrastructure for businesses, offering APIs, merchant solutions, and digital wallets that allow enterprises to scale operations across Nigeria and other African markets. This positions the company within broader African fintech trends, where payments, mobile wallets, and enterprise infrastructure are driving the continent’s digital shift.

What distinguishes Paga is its dual approach of solving immediate transactional challenges for everyday users while simultaneously building a Pan-African financial ecosystem.

By enabling fast, secure payments and integrating unbanked populations into the digital economy, Oviosu is laying the groundwork for financial inclusion that transcends national borders.

Paga’s evolution reflects a clear strategy to transform Africa’s fragmented payment landscape into a connected, technology-driven platform that supports both individuals and businesses, creating systemic impact across the continent.

Early Life, Education, and Experience

Eyitayo “Tayo” David Oviosu was born on 10 September 1977 in Lagos State, Nigeria. He is ethnically from Edo State and was raised in a single-parent home by his mother, who brought up five boys on her own. At the age of 16, he moved to the United States, where he would continue his education and lay the foundation for his future entrepreneurial journey.

Oviosu pursued a Bachelor of Science in Electrical Engineering (cum laude) at the University of Southern California (USC). During his undergraduate studies, he faced significant financial and academic challenges, often holding multiple jobs to support himself, demonstrating early resilience and discipline.

After graduating, Oviosu began his professional career as a chip design engineer at Biomorphic VLSI in Los Angeles. He worked on designing a digital imaging chip that was fabricated in Taiwan. However, the first version of the chip failed, and Oviosu was let go after three months a pivotal moment that taught him the importance of resilience, problem-solving, and learning from failure.

He then worked as a software engineer at a Los Angeles–based startup and briefly took on temporary roles to sustain himself.

Oviosu later joined Deloitte Consulting as a Senior Consultant in the CRM and Technology practice. There, he led project teams across telecom, high-tech, government, pharmacy, and healthcare sectors, gaining extensive experience in strategy, implementation, and client management.

Seeking to expand his strategic and business knowledge, he enrolled at Stanford Graduate School of Business, earning an MBA in 2005. During his time at Stanford, he deepened his understanding of corporate strategy, operations, and entrepreneurial finance.

After business school, Oviosu joined Cisco Systems as Manager of Corporate Development. In this role, he oversaw corporate strategy, acquisitions, and private-equity investments, including supporting Cisco’s expansion into Africa. This experience exposed him to high-level negotiations, mergers, and international business operations.

In 2008, he returned to Nigeria to serve as Vice President at Travant Capital Partners, a West African private-equity firm, deepening his understanding of African markets and investment dynamics. Around the same time, he co-founded Kairos Angels, an angel investment club supporting early-stage African entrepreneurs.

Across these stages in engineering challenges, consulting work, corporate development and private equity, Oviosu accumulated a rare combination of technical expertise, strategic insight, and deep African market knowledge. This blend of engineering precision and business strategy uniquely positioned him to build Paga with both technological depth and continental vision.

These layers of experience became the foundation for Paga, allowing him to approach financial technology in Africa with both technical rigor and a clear understanding of the systemic barriers to financial inclusion.

Inspiration to Start Paga

Tayo Oviosu’s inspiration for founding Paga in 2009 was deeply personal, born out of his frustration with handling cash. As he told The Guardian Nigeria, “I founded Paga … out of the frustration of carrying cash around.” Despite having multiple bank accounts, card payments were unreliable: ATMs and PoS terminals frequently failed or were inconvenient.

At the time, Nigeria’s banking infrastructure was slow, fragile, and concentrated in urban areas, making a digital alternative both timely and urgently needed.

What began as a personal pain point soon revealed a larger structural challenge: millions of Nigerians lacked access to formal financial services. Oviosu framed Paga’s mission around two core problems “making it easy for people to pay and get paid … and delivering financial services to the mass market.” He understood early that true scale required more than an app; it required physical infrastructure and an ecosystem approach.

When it came to raising funds, Oviosu didn’t sugarcoat the difficulty. “the ‘use of cash’ problem was not going to be solved without significant investment.” he said. He knew the vision needed long-term capital to build agents, technology, and an operational footprint across the country.

His ambition also carried a continental, even global dimension. In a TechCabal interview, he said, “I certainly did not set out to just try something. I set out to build a business that I believe will have a massive impact on Nigeria … As I got going, I quickly realised that the problems I set out to solve were global.” He emphasized that Paga was not just a payments company, but a financial infrastructure platform enabling developers and companies via open APIs.

This vision led to Paga’s hybrid model, a nationwide network of agents (kiosks, small shops) paired with a digital wallet, enabling deposits, withdrawals, transfers, and payments even for people without smartphones or bank accounts. Unlike early mobile-money competitors that leaned heavily on telcos, Paga built a neutral, open, agent-driven system accessible to anyone.

Ultimately, Oviosu’s inspiration was a blend of personal frustration and a bold social mission: to build a digital financial system that works for everyone in Nigeria and eventually across Africa. His conviction went beyond making payments easier. He aimed at driving universal financial inclusion through scalable, agent-based infrastructure.

What Problem Paga Solves

Paga was created to confront a deeply entrenched challenge in Nigeria (and many African markets). The dominance of cash, which limits access to formal financial services, raises transaction costs, and excludes large segments of the population from efficient, secure money movement. Over time, Paga has evolved into a multi-service fintech platform that addresses these systemic issues through payments, infrastructure, and inclusion.

Paga’s model directly tackles Nigeria’s core financial barriers by bridging cash reliance, limited infrastructure, and slow legacy systems.

1. Cash Dependence and Low Financial Inclusion

A large portion of Nigeria’s population remains unbanked or underbanked, relying heavily on cash for daily transactions. Through its mobile wallet and agent network, Paga allows people to deposit and withdraw cash locally, then transact digitally bringing users without bank accounts or smartphones into the formal financial system.

2. High Cost and Risk of Handling Cash

Managing physical cash is costly, risky, and inefficient for both individuals and businesses. By digitizing value through wallets, Paga reduces the need to carry or store cash, lowering exposure to theft and cutting friction. As Oviosu noted during Paga’s 10-year celebration, “storing money digitally … significantly reduces friction [and] transaction costs.”

3. Fragmented or Inaccessible Digital Infrastructure

Many digital services remain unavailable in rural areas or too costly for mass-market users. Traditional banks also lack a wide rural presence. Paga’s hybrid model of local agents paired with digital channels (app, USSD) gives users multiple entry points. Today, its ecosystem includes the Paga consumer wallet, “Paga Engine” for businesses, and Doroki for SME retail.

4. Slow Settlement and Liquidity Issues for Businesses

In conventional banking, transfers often settle in T+1 or T+2, meaning businesses wait one or two days to access funds. By contrast, Paga Engine enables near-instant movement recipients receive money in under three seconds, improving liquidity and operational flow.

5. Limited Access to Financial Infrastructure for Fintechs and SMEs

Smaller businesses and emerging fintechs often lack the backend rails wallets, switching systems, payment APIs needed to build their services. Paga offers infrastructure-as-a-service to over 150 businesses, allowing them to embed payments and financial services directly into their products.

6. Security and Trust Issues

In cash-driven economies, trust is a major concern. Paga employs multiple security layers and is PCI DSS certified, meeting global standards for data protection and safeguarding user accounts.

Milestones Achieved to Date

Paga’s journey from a small payments startup to a fintech infrastructure powerhouse is marked by measurable impact.

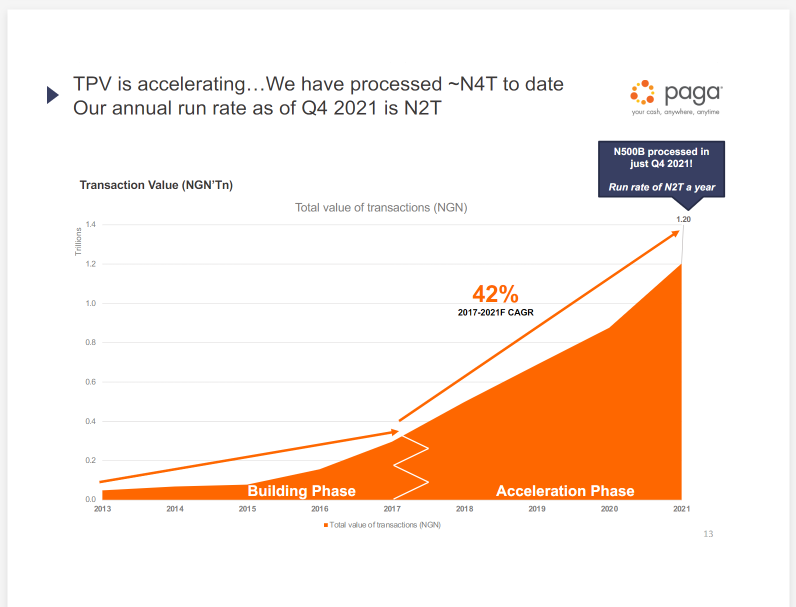

Since its founding in 2009, the company has processed 460 million transactions worth approximately ₦23 trillion (~ US$44 billion) over 16 years, reflecting rapid adoption and growth.

By early 2025, Paga had over 29 million registered users, underscoring its scale and reach across Nigeria. Its agent network also ranks among the country’s largest, comparable in footprint to Opay and MTN MoMo but with a stronger infrastructure-driven focus.

Beyond user numbers, Paga has generated tangible economic value. The company has created around 1,000 direct jobs, while its extensive agent network supports about 100,000 indirect jobs, enabling financial access in underserved areas.

Over the years, Paga expanded its offerings beyond consumer payments. It launched Platform-as-a-Service (PaaS), allowing businesses to integrate Paga’s infrastructure into their operations.

As of 2025, about 150 businesses relied on the platform to power payments, collections, and other financial services.

In June 2025, Paga unveiled Doroki, a cloud-based business management tool for SMEs helping shops track inventory, reconcile payments, manage customers, and access analytics.

A typical user might be a local grocery or pharmacy that needs simple tools to monitor daily cash flow. The tool also works offline, syncing when internet connectivity returns, and aims to onboard thousands of businesses within one year.

Security and reliability have been central to Paga’s growth. The platform is PCI DSS certified, ensuring globally recognized standards for financial security. Real-time settlements through Paga Engine allow businesses and individuals to transfer funds in seconds, improving liquidity and operational efficiency.

Paga’s contribution to international remittances is significant. By 2025, it had partnered with 18 remittance companies, handling US$4.4 billion in remittance volume over the past year. In a country where diaspora remittances often surpass oil revenue, this represents a major role in Nigeria’s financial inflows.

Recognition of Paga’s impact has grown alongside its operational milestones. In May 2025, the company was named among Africa’s Fastest-Growing Companies by the Financial Times and Statista for the third consecutive year. It continues to create both direct and indirect jobs while enabling financial inclusion on a massive scale.

Across 16 years, Paga has evolved from a mobile-money experiment into a foundational pillar of Nigeria’s financial ecosystem. Its growth is measured not only in transactions or users but also in job creation, enterprise infrastructure, and broader economic digitization.

Strategic expansions into remittances, SME tools, and platform services demonstrate its transformation from a fintech startup into a mission-driven engine for financial inclusion and systemic innovation.

Lessons for Other African Entrepreneurs

Paga’s journey provides strategic lessons for founders operating in emerging markets. Tayo Oviosu’s experience building Paga demonstrates how disciplined execution, user-centric design, and strategic thinking can transform an idea into a pan-African financial ecosystem.

1. Stick to the Mission Through Challenges

Building a business that addresses structural problems, such as financial inclusion, requires persistence. Oviosu emphasizes resilience: “There’s always a behaviour change required, which takes time. Resilience and belief in your mission are vital.” This mindset helped Paga navigate regulatory hurdles, scale steadily, and form productive partnerships with regulators, a critical factor in African fintech success.

2. Build and Own Your Platform

Paga chose to develop its own technology infrastructure rather than relying solely on third-party solutions. Owning the platform allowed better control, scalability, and security. Hiring the right technical talent and maintaining system integrity remain critical for long-term success.

3. Base Decisions on Strategy, Not Just Instinct

While intuition can guide early choices, Oviosu stresses aligning every decision with a clear three-to-five-year strategy. This approach ensured Paga’s growth remained focused and sustainable rather than reactive.

4. Leverage Relationships and Partnerships

Early Paga success relied on trusted networks like friends, colleagues, and advisors who shared the vision. Building strong, trust-based relationships, including with regulators and ecosystem partners, is essential for scaling ventures across Africa.

5. Focus on the Underserved and Adapt Models While Scaling

Paga’s agent network and USSD-enabled wallet show that serving populations traditionally excluded from financial services can drive impact and growth. The company evolved from a mobile-wallet app into a three-arm ecosystem consumer payments, platform infrastructure, and SME tools like Doroki demonstrating the value of modular, adaptable business models.

6. Raise Capital IntentionallyFundraising should align with a long-term vision. Early investors were collaborators who believed in the mission, not just financial returns. Raising money carefully, and ensuring investor alignment, reduces distractions and maintains strategic focus.

Across these lessons, Oviosu’s journey illustrates the combination of vision, strategic execution, and operational discipline required to scale African ventures successfully. Entrepreneurs who apply these principles can build resilient, impactful businesses capable of driving systemic change across the continent.

Tayo Oviosu’s journey with Paga shows how a clear mission, combined with technical expertise and strategic execution, can transform a simple idea into a system-wide solution for financial inclusion. By addressing both everyday transactional challenges and enterprise infrastructure needs, Paga has become a cornerstone of Nigeria’s digital economy, creating jobs, enabling businesses, and bridging gaps in financial access for millions.

As Paga continues to expand across Africa, its focus on scalable, agent-driven infrastructure and innovative financial tools positions it to redefine the continent’s digital payment landscape and bring universal financial access closer to reality. With plans to enter additional African markets and deepen enterprise infrastructure, Paga’s growth potential remains vast.

Oviosu’s legacy is one of vision, resilience, and transformative impact, with Paga serving as a model for how African fintechs can drive systemic change and accelerate the continent’s digital economy.

{kind=link}