Table of Contents

The four fastest-growing container trade lanes in the world are now all connected with Africa. Sub-Sahara Africa is posting the strongest regional import growth globally at 17.1% year-to-date. That matters because shipping lines do not add capacity at this pace for a temporary spike. They do it when they believe trade patterns are shifting structurally.

The clearest signal is on the Asia-Africa trade itself. Alphaliner data show fleet capacity on Asia-Africa services rose to nearly 2.2 million twenty-foot equivalent units (TEUs) in late 2025, up 54.3% year on year from 1.4 million. To meet this demand, Mediterranean Shipping Company (MSC), a Swiss-based global leader in container shipping and logistics, began using massive 24,000-TEU ships on its Africa Express service, stopping at ports like Lomé, Tema, Abidjan, and Kribi. This major investment proves that global shipping companies expect African import demand to stay strong for the long term.

That demand surge is colliding with a stubborn scale gap. Only four African ports made Lloyd’s List’s 2025 global top 100 container ports: Tanger Med, Port Said, Alexandria and Lomé. Even Durban, which handled 4.5 million TEU, fell out of the ranking because congestion, vessel delays and weak rail connectivity dragged down performance.

For investors, the message is clear: Africa's trade is growing faster than its ability to move goods smoothly. The best opportunities are no longer just about handling more cargo. Instead, the real value is in ports and trade routes that can connect large ship capacity with fast, reliable transport to the interior of the continent.

Mombasa vs. Dar Es Salaam: Which Corridor Will Capture The Next Wave Of Investment?

Mombasa enters this race from a position of measurable strength. Kenya Ports Authority says the port handled a record 45.45 million tonnes in 2025, with container traffic up to 2.11 million TEU and transit cargo up 19.5% to 15.88 million tonnes.

The rise in transit cargo is critical. It shows the Northern Corridor still attracts more goods for Uganda, Rwanda, and Burundi than its rivals. To keep this lead, Kenya is adding 1.4 million TEU of capacity by expanding berths 19B, 23, and 24. Meanwhile, the Port of Lamu is emerging as a second major trade hub, handling 799,161 tonnes and 55,687 TEUs in 2025.

Mombasa is upgrading its systems and automating gates to speed up operations. However, the real challenge is now time, not just berth capacity. Kenya is launching a digital Port Community System to link shipping lines, agents, transporters, and government agencies with the aim of cutting cargo clearance times by 30%. This is vital since current delays average 13.5 days. For inland customers in Uganda, Rwanda, and Burundi, reducing these delays is as valuable as adding new equipment because it provides the end-to-end predictability they need.

Dar es Salaam is quickly becoming more efficient. The port handled 27.7 million tonnes in 2024/25, up from 23.69 million. Its regional reach is growing, serving the DRC (6 million tonnes), Zambia (3.5M), and Rwanda (1.7M). Through the Dar es Salaam Maritime Gateway Project, the port deepened its berths to 14.5 metres which cut average vessel stay times from ten days to three. By adding the Kwala Inland Container Depot and a new rail link to boost capacity up to 480,000 TEUs from 300,000 TEUs, Tanzania is proving that success depends on matching port speed with fast inland transport.

Mombasa holds the lead in East Africa's regional trade, proven by its transit growth and the rise of Lamu as a secondary hub. However, Dar es Salaam is quickly closing the gap by improving efficiency, specifically reducing vessel delays, improving berth predictability, and enhancing digital coordination. The competition is no longer about port quay length alone, but about whether the Northern Corridor road and rail reforms can preserve Mombasa’s incumbency faster than the Central Corridor converts Dar’s berth-side port-side gains into efficient inland transport. The port that wins this race will capture the significant logistics, warehousing, and industrial investment decisions that follow.

How Is Lekki Deep Sea Port Reshaping Competitive Shipping In West Africa?

Lekki Deep Sea Port has changed the competitive baseline in Nigeria by offering the modern, automated, deepwater capacity that older ports like Lagos lacked.

Lekki has already reached nearly 50% of its designed operational capacity, with volume growing every month. Phase 1 handles 2.5 million TEUs annually, with plans to expand to 6 million TEUs.

That is significant for a port built as a fully automated deepwater terminal rather than an upgrade. Lekki’s main bottleneck is no longer berth space. Its managing director says the constraints are customs integration, physical examinations, rail access and evacuation links. In other words, the port can receive cargo faster than the wider system can clear it. Even so, for operators, managing high volume is a better challenge than the standard equipment shortages previously seen at Apapa.

Lekki isn’t the uncontested winner in the region. Abidjan remains a powerful competitor and handled 46.6 million tonnes and 1.6 million TEU in 2025. According to Ecofin, its trade with Mali grew by 76.4% and Burkina Faso by 16.6%. Unlike newer terminals, Abidjan is already a proven gateway for the Sahel, reliably moving both containers and traditional cargo.

Lekki offers deeper water and automation compared to older ports. However, the port’s management notes that barges still handle very little cargo. Without better customs digitalization and better road and rail links, the cost benefits of its deepwater capacity will be lost to traffic at the gate. As a result, the competition in West Africa is moving further inland.

Abidjan still moves fewer containers than transshipment hubs like Tema and Lomé. Lekki's competitive edge is the opportunity to combine serving Nigeria’s huge local market with becoming a major regional transshipment center. The shipping market is ready for this transition as proven by the arrival of massive 24,000-TEU MSC ships in West Africa. However, Lekki's long-term success depends less on the terminal and more on Lagos improving the supporting infrastructure, specifically customs, rail, and barge connectivity.

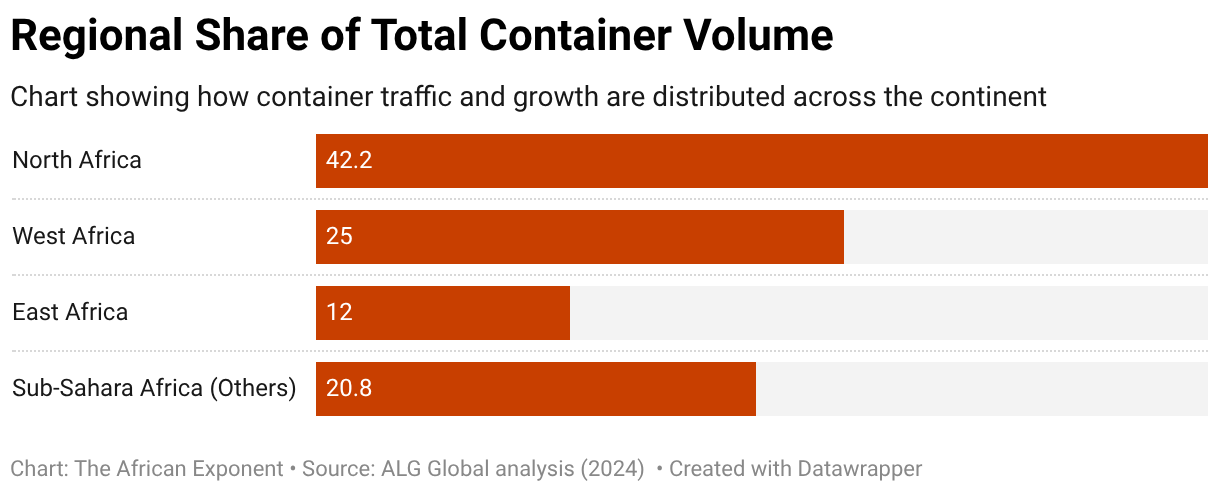

Can Sub-Saharan Hubs Close the North African Scale Gap?

North Africa leads the continent in shipping volume, handling 42.2% of all container trade, West Africa about 25% and East Africa 12%. The North African success is driven by its prime location near Europe and major global trade routes. Tanger Med is the top performer, handling over 11.1 million TEUs and 161 million tonnes of cargo in 2025 alone.

Can Sub-Saharan African ports copy this success? Partly. While they lack Tanger Med's location on the Strait of Gibraltar, they can adopt its strategy which includes deepening channels, expanding terminals early, linking ports to road and rail, and digitizing customs.

Dar es Salaam and Mombasa are modernizing through digital systems and automation. However, Lekki’s experience shows that fast quay automation is useless if customs and inland transport remain slow or disorganized. Sub-Saharan ports must act as efficient network hubs, not just national gateways, to avoid staying structurally small despite high growth.

Where Are the Real Opportunities in Africa Port Capacity Race?

Winning African corridors are focused on reducing overall logistics delays, not just adding berth capacity. Mombasa is defending its position with new capacity and digital reform, while Dar es Salaam gains ground by cutting vessel time and improving inland transport. Lekki has modern port technology but still needs faster customs, rail, and barges to convert its capacity into a true advantage. Tanger Med serves as the benchmark because it fixed the full system, not just the waterfront infrastructure.

AfCFTA raises the stakes, because higher intra-African trade will reward ports that can move goods inland cheaply and predictably. South Africa’s Durban–Gauteng corridor is the cautionary case. Rail carries less than 14% of freight on the corridor against a national target of 50%. Daily trains reportedly fell from 80 to 15 by 2023–24. The crisis is so severe that a R50 billion "Port of Gauteng" has been proposed to fix the link between the coast and hinterland.

For investors and operators, the key takeaway is to back regions where inland connectivity improves as quickly as port capacity. In East Africa, watch if Dar es Salaam can match Mombasa's reliability and new capacity before it locks in the lead. In West Africa, Lekki's success depends on how fast its road and rail links modernize. While new docks get the attention, the real winners will be those with the best rail access, truck turnarounds, and digital customs.

{kind=link}