Table of Contents

Africa’s air cargo market is expanding faster than almost anywhere in the world, but the headline growth numbers hide a more complicated reality. According to the International Air Transport Association (IATA) November 2025 Air Cargo Market Analysis, African carriers increased freight volumes by 15.6% year-on-year, faster than those in Asia-Pacific, Europe, or North America. On paper, this signals strong market expansion, yet most cargo planes flying from Africa still leave with large portions of their capacity unused.

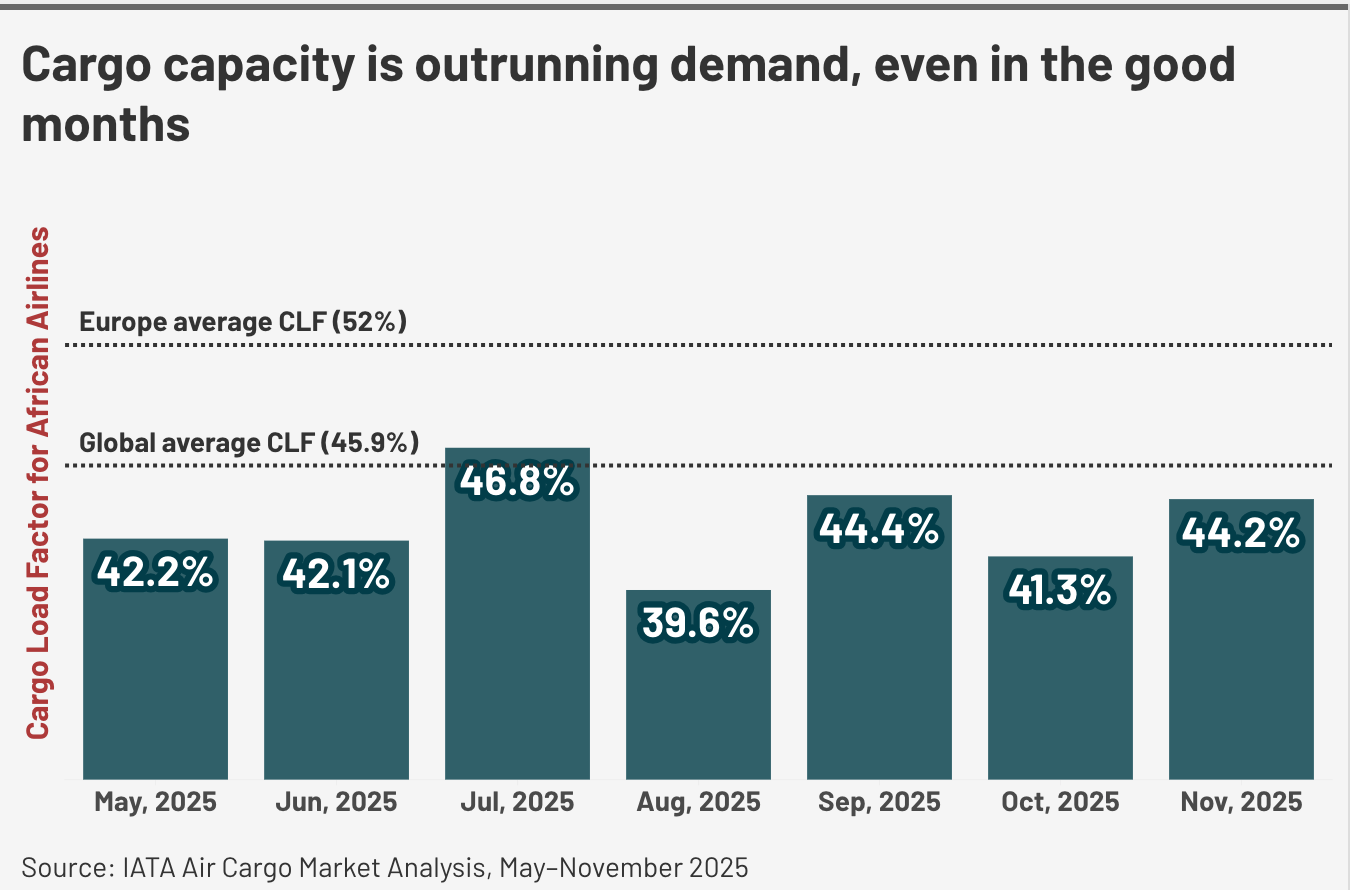

Cargo capacity on African airlines grew even faster than freight demand. Available cargo space increased by 18.2%, leaving airlines filling only 44.2% of the cargo space available on their aircraft. For investors and industry observers, the key question is whether airlines are expanding in anticipation of Africa’s growing trade or adding capacity faster than the market can absorb.

This article examines the numbers behind Africa’s cargo boom and explains why one of the world’s fastest-growing air freight markets still struggles to fill its planes.

Why Are African Airlines Adding Cargo Space When Current Planes Aren’t Full?

At first glance, expanding cargo capacity while planes remain partially empty may seem risky. However, the decision reflects a long-term bet on Africa’s growing trade volumes.

Over the past decade, air freight demand across the continent has grown steadily. According to IATA market analysis reports covering 2015-2025, African air cargo demand expanded at an average annual rate of approximately 4-6%, consistently exceeding global averages in several years. This steady growth has encouraged airlines to invest in new cargo capacity in anticipation of future demand.

Trade developments across the continent also support this expansion. The African Continental Free Trade Area (AfCFTA), which began implementation in 2021, is gradually increasing cross-border trade between African economies. As tariffs fall and logistics networks improve, companies are moving more goods between regional markets, many of which rely on air transport for speed and reliability.

Export industries are also driving demand for air freight. Kenya’s flower sector provides a clear example. The country exported more than 200,000 tonnes of cut flowers annually in recent years, with approximately 70% shipped to Europe, according to the Kenya Flower Council. Because flowers are highly perishable, most of these exports travel by air from Nairobi’s Jomo Kenyatta International Airport to European markets.

South Africa’s pharmaceutical sector shows a similar pattern. The country exported hundreds of millions of dollars’ worth of pharmaceutical products annually, according to trade data. Many high-value medical products and vaccines rely on temperature-controlled air transport to reach international markets quickly.

Infrastructure investments are reinforcing this trend. Several African aviation hubs have expanded their cargo facilities in recent years. Ethiopian Airlines, for example, developed one of the continent’s largest cargo terminals in Addis Ababa with a capacity of around one million tonnes per year, designed to handle pharmaceuticals, perishables, and other sensitive cargo. Airports in Nairobi, Johannesburg, and Lagos have also upgraded their cold-chain logistics and cargo-handling systems.

Together, these developments show that African airlines are not expanding cargo capacity randomly. They are positioning themselves for a market they expect to grow significantly over the coming decade.

Why Are African Airlines Struggling to Fill Their Cargo Planes?

Despite this growth, African airlines still face a major challenge, much of the cargo space they add remains unused.

One of the key measures in the aviation industry is the Cargo Load Factor, defined as the percentage of available cargo space on an aircraft that is filled with freight. A higher load factor means planes are carrying more cargo relative to their total capacity.

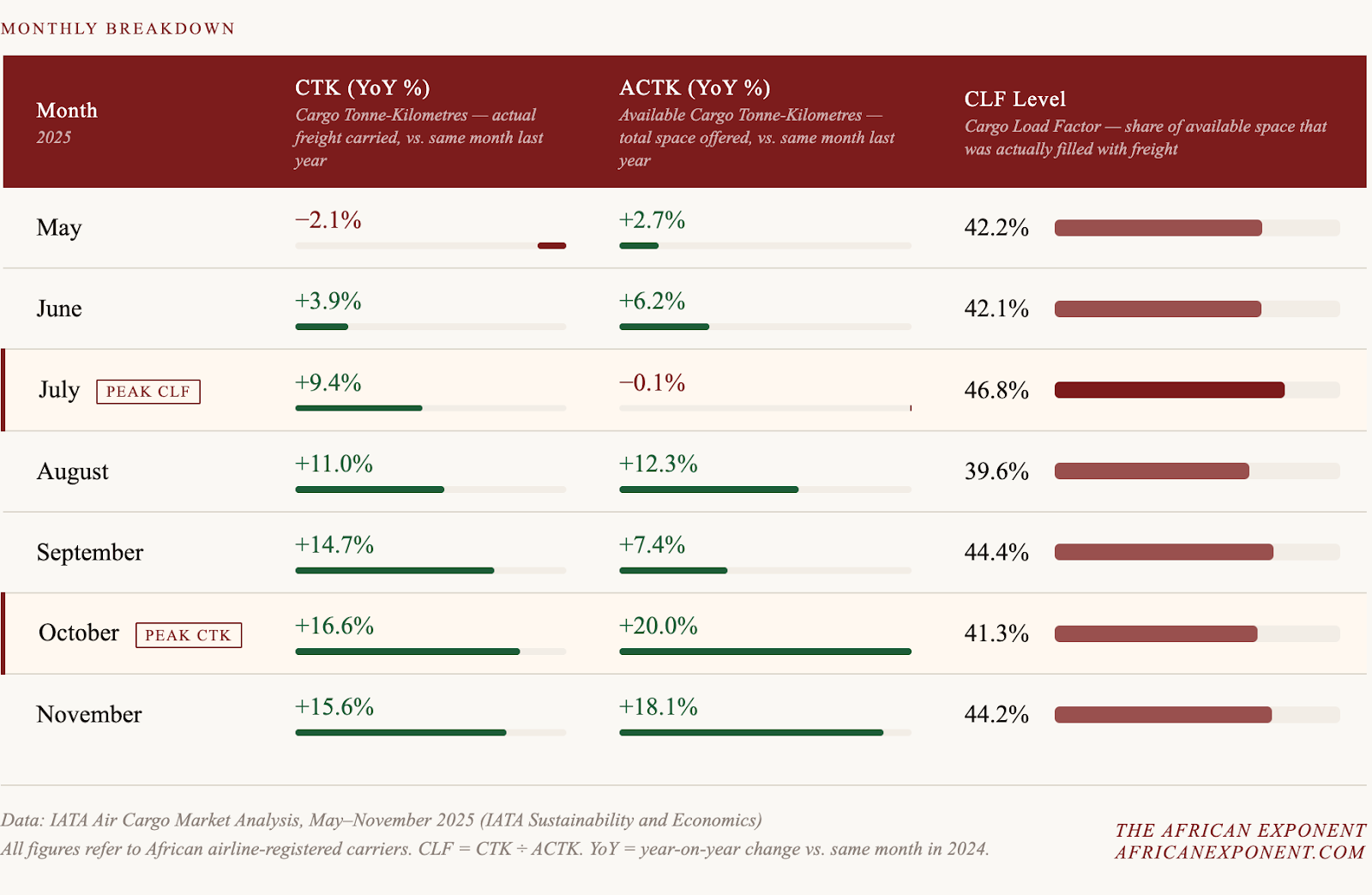

In Africa, this number remains relatively low. According to IATA’s November 2025 data, African airlines recorded a cargo load factor of 44.2%, compared with a global average of 49.1% and 57.9% in Europe.

In practical terms, this means that nearly half of the cargo space on African aircraft often flies empty. While demand for air freight is growing, the expansion of cargo capacity is happening even faster.

Monthly data throughout 2025 shows that this pattern has been relatively consistent rather than a one-time anomaly. Although freight volumes increased during the year, the amount of available cargo space also rose as airlines added aircraft, routes, and freighter capacity. As a result, the gap between supply and demand remained visible across several months of IATA’s air cargo market reports.

Fleet structure also contributes to these regional averages. Ethiopian Airlines, Africa’s largest cargo operator, maintains one of the continent’s most extensive dedicated freighter fleets, including Boeing 777 and Boeing 767 cargo aircraft. The airline operates global cargo routes connecting Africa with Europe, Asia, and the Middle East, transporting large volumes of freight through its Addis Ababa hub.

Because Ethiopian Airlines handles a significant share of the continent’s long-haul cargo traffic, its performance can influence regional averages. However, many other African carriers operate with smaller cargo fleets or rely primarily on the cargo space available in passenger aircraft. This makes it more difficult for them to maintain consistently high cargo load factors.

Market conditions also affect profitability. Industry freight indexes show that global air cargo spot rates in 2025 frequently hovered in the mid‑to‑low single digits per kilogram across key trade lanes. For example, the WorldACD index reported a global average spot rate of about $2.65/kg at the start of 2025, with variations across regions and routes. While these rates remained relatively stable compared with the previous year, airlines continued to face volatile jet fuel prices and rising operational costs.

For airlines operating with partially filled cargo holds, these pressures can make profitability difficult even when freight volumes are growing.

If Airlines Are Struggling, Who Actually Benefits from Africa’s Air Cargo Growth?

If African airlines are adding capacity faster than demand, the immediate question for investors is: who profits from the continent’s growing air cargo market? The answer lies not with the airlines themselves, but with the ecosystem surrounding them.

Freight forwarders play a critical role in consolidating shipments from multiple businesses before cargo is transported by air. By combining goods from different clients into single shipments, forwarders help airlines use space more efficiently while capturing significant value within the logistics chain. Global companies such as DHL Global Forwarding, Kuehne + Nagel, and Bolloré Logistics have expanded operations across Africa to meet this growing demand. A strong real-world example comes from DHL Group, which in October 2025 announced a landmark investment of over €300 million (approximately $325 million) specifically for Sub-Saharan Africa. This investment targeted both DHL Global Forwarding, expanding cold-chain capabilities for perishables like fruit, flowers, and pharmaceuticals, and DHL Supply Chain, building new warehouses to support the “last mile” of e-commerce. These moves demonstrate that forwarders are not only responding to current growth but are also making long-term bets on Africa’s air cargo market, creating tangible opportunities for investors beyond the airlines themselves.

Ground handling companies also capture value. Every shipment passes through loading, unloading, customs processing, and storage at major hubs, which allows operators to earn revenue regardless of which airline carries the freight. Companies such as Swissport, Ethiopian Cargo Handling, and NAS (National Aviation Services) provide consistent returns even when planes fly underfilled. For instance, Ethiopian Cargo Handling has invested in advanced cold storage facilities at Addis Ababa Bole International Airport to manage the increasing volume of perishables and pharmaceutical shipments.

Cold chain logistics operators benefit from Africa’s growing pharmaceutical and agricultural exports. Temperature-controlled transport is essential for products such as vaccines, biologics, flowers, and fresh produce. Hubs in Nairobi, Addis Ababa, and Johannesburg are expanding cold storage, refrigeration, and transport infrastructure to meet rising demand. Companies like DHL Global Forwarding, Bolloré Logistics, and local operators such as ColdHubs are positioning themselves to profit from this growth, independent of airline performance.

Looking ahead, investors should watch several key signals. The AfCFTA’s trade growth, ongoing airport and cargo infrastructure expansions, and the increasing adoption of cold chain solutions will continue to drive demand across the continent. By focusing on these areas, investors can access growth without assuming the direct risks airlines face, making the broader logistics ecosystem a more reliable way to capture Africa’s expanding air cargo market.