Table of Contents

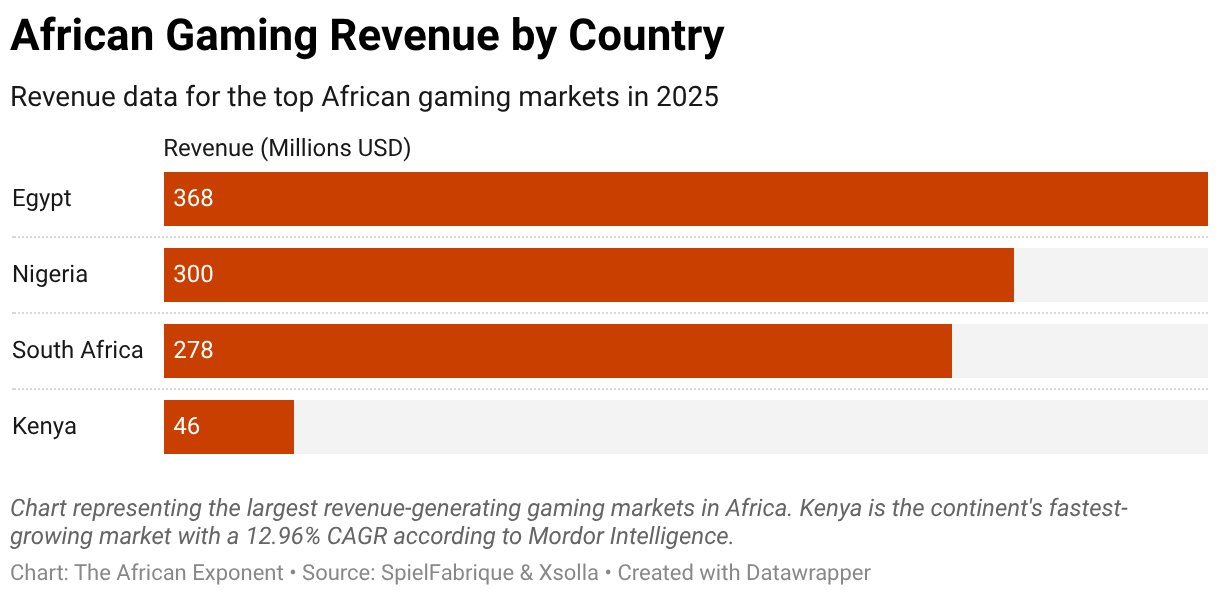

According to the SpielFabrique & Xsolla “State of the African Video Game Industry 2026” research, Africa’s gaming market surpassed $2.29 billion in 2025 revenue. It is growing at 12% each year, which is six times faster than the rest of the world. Top markets by revenue include Egypt ($368M), Nigeria ($300M), South Africa ($278M), and Kenya ($46M). There are now roughly 349 million gamers on the continent, and 90% of them play on mobile phones. Even though the market is expanding rapidly, the lack of easy-to-access payment systems remains the biggest hurdle to turning this huge player base into a high-revenue industry.

The continent's immense potential for gaming monetization is clearly reflected in its long-term market forecasts. Recent projections indicate that the African gaming market will reach $4.10 billion by 2031, with a user base exceeding 400 million by 2027. While Africa has the audience, the engagement and the mobile distribution habits of major gaming regions, revenue capture still lags because too many African players reach the game but cannot complete the transaction.

Why Does Africa’s Gaming Boom Still Fail at Checkout?

The African gaming industry now has the scale of a serious market but the monetization architecture is lacking or limited. The gargantuan imbalance between the gaming audience and gaming revenue is too wide to explain by content quality or consumer interest alone. It points instead to a structural barrier in how players are asked to pay. Africa’s gaming story is therefore not mainly about user acquisition anymore, it is about why so many users still sit outside the established transaction layer.

The first constraint is financial exclusion built into the dominant gaming business model. Global gaming monetization was designed around card-linked app stores, seamless in-app purchases and users with stored digital payment credentials. That friction becomes apparent at the app-store layer. While Google Play is the most common way for African developers to reach gamers in the continent, the platform still relies heavily on credit cards for billing. But since most people across the continent do not have access to credit cards, many players are unable to complete their purchases.

In Africa, where transactions often run through mobile money, airtime, agent networks and local wallets, the store becomes a conversion bottleneck. Users can enjoy free tier games until it is time to upgrade and they have no viable payment methods on the purchase screen. That is where much of the continent’s gaming revenue still disappears.

Across Egypt, Kenya, Nigeria and South Africa, the top payment options include credit cards, mobile money, Google Pay, and airtime, but their degree of utilization varies by country. Kenya is the clearest example: mobile money reaches 67% usage, far above the cross-market average. Egypt leans more toward credit cards and Google Pay. Nigeria shows stronger airtime usage. The implication for operators is straightforward. There is no continental payment switch. Monetization in Africa remains patchy because payment behavior is country-specific, and companies that fail to localize at that level are effectively choosing lower conversion and revenues.

Which Companies Are Working on Fixing Gaming Payments?

The companies best positioned to capture value in African gaming are the ones solving transaction friction, not simply producing content. Carry1st is the clearest example because it sits at the intersection of publishing, payments and distribution. Through Pay1st and the Carry1st Shop, it allows players to buy in-game currency and game passes using local payment methods and local currency rather than relying entirely on conventional app-store payment rails.

That is a materially different value proposition from standard publishing. It reduces friction between intent and transaction, which is where African gaming still leaks revenue. Carry1st’s competitive edge is therefore structural since it sits closer to the payment bottleneck than most content businesses do.

Xsolla occupies a different strategic position. Unlike Carry1st, its core strength is not being Africa-native but being a global gaming commerce infrastructure provider that can localize payments at scale. For international publishers, that matters. Africa remains attractive as a growth market, but most large publishers do not want to build country-by-country payment operations from scratch. Xsolla’s relevance lies in reducing that market-entry cost. The platform’s main goal is to help international game companies successfully handle payments in Africa. It is not the most local option but it serves as the most scalable way to connect global content with the specific payment methods used by African customers.

Gara Store is the best example of a local challenge to the current app-store model. It was built on the premise that mainstream stores do not fit African payment behavior or African creator economics. That makes Gara strategically significant even at smaller scale. It is not just another distribution platform but an attempt to create an African-native commercial route for African-made content. Its proposition is sharper because it addresses both sides of the market at once, discoverability for local creators and payment compatibility for local users. Its challenge, however, is obvious. Relevance is not the same as scale, and Gara still has to overcome the trust, device integration and reach advantages of Google Play and OEM ecosystems. The long-term success of Gara depends on whether payment-fit can eventually beat incumbency of known platforms.

How Does Africa’s Weak Video Game Monetization Affect The Content It Produces?

African studios’ preference for international markets is often described as a creative choice. In reality, it is mainly a financial one. When local players are hard to monetize because of payment friction, developers reduce this risk by targeting users in markets where checkout is smoother, card penetration is higher and spending is easier to capture. The SpielFabrique/Xsolla reporting reveals that many African studios prioritize global markets over local audiences because domestic monetization remains limited. That does not point to a failure of ambition. It is a rational response to non-existent/limited monetization infrastructure at home.

But rational short-term strategy can still create a long-term development problem. When studios design first for export, they are more likely to optimize for genres, aesthetics and monetization systems already working in foreign markets. That can generate revenue, but it also weakens the pipeline for Afrocentric intellectual property. A market that cannot reliably monetize local audiences will struggle to sustain creators who build local narratives for those audiences. In that regard, the monetization gap does not just shape payments but also shapes the games being made.

This dilemma matters because the audience is already signaling demand for representation. GeoPoll found that more than half of respondents agreed that cultural relevance matters in games. 44% said there are not enough games with characters who look like them or reflect their environment. The commercial message becomes clear that local representation is not merely a cultural aspiration but an identifiable demand signal. Yet until payment infrastructure improves, that demand will remain harder to convert into sustainable returns for the studios best placed to serve it.

What Comes Next: The Next Winner Will Be the Company That Converts Reach Into Revenue

The next phase of African gaming growth will depend less on adding players than on deepening monetization per player. For example, cloud gaming presents a new frontier. According to the SpielFabrique/Xsolla report, it is the fastest-growing segment, expanding at roughly 14% CAGR. It reduces the need for expensive consoles and allows more users to access premium games with their current devices. However, cloud gaming still relies primarily on credit cards to process payments, making it inaccessible to most African gamers. Companies that fix this payment barrier are therefore best positioned to capture revenue from this fast-growing cloud audience.

Investors and operators should focus on the payment layer. The market has the players, but it needs a better way to collect payments. Companies that simplify local billing and distribution will be the most successful in the long-run.

{kind=link}