Table of Contents

For most of the 2000s and 2010s, Israeli arms transfers to Africa remained relatively limited, often recorded in low volumes according to data from the Stockholm International Peace Research Institute (SIPRI). That pattern has changed sharply in recent years.

SIPRI classifies “major arms” as high-value military systems such as drones, air defense platforms, radar systems, and missile technologies. These systems require continuous maintenance, software updates, training, and technical support to remain operational.

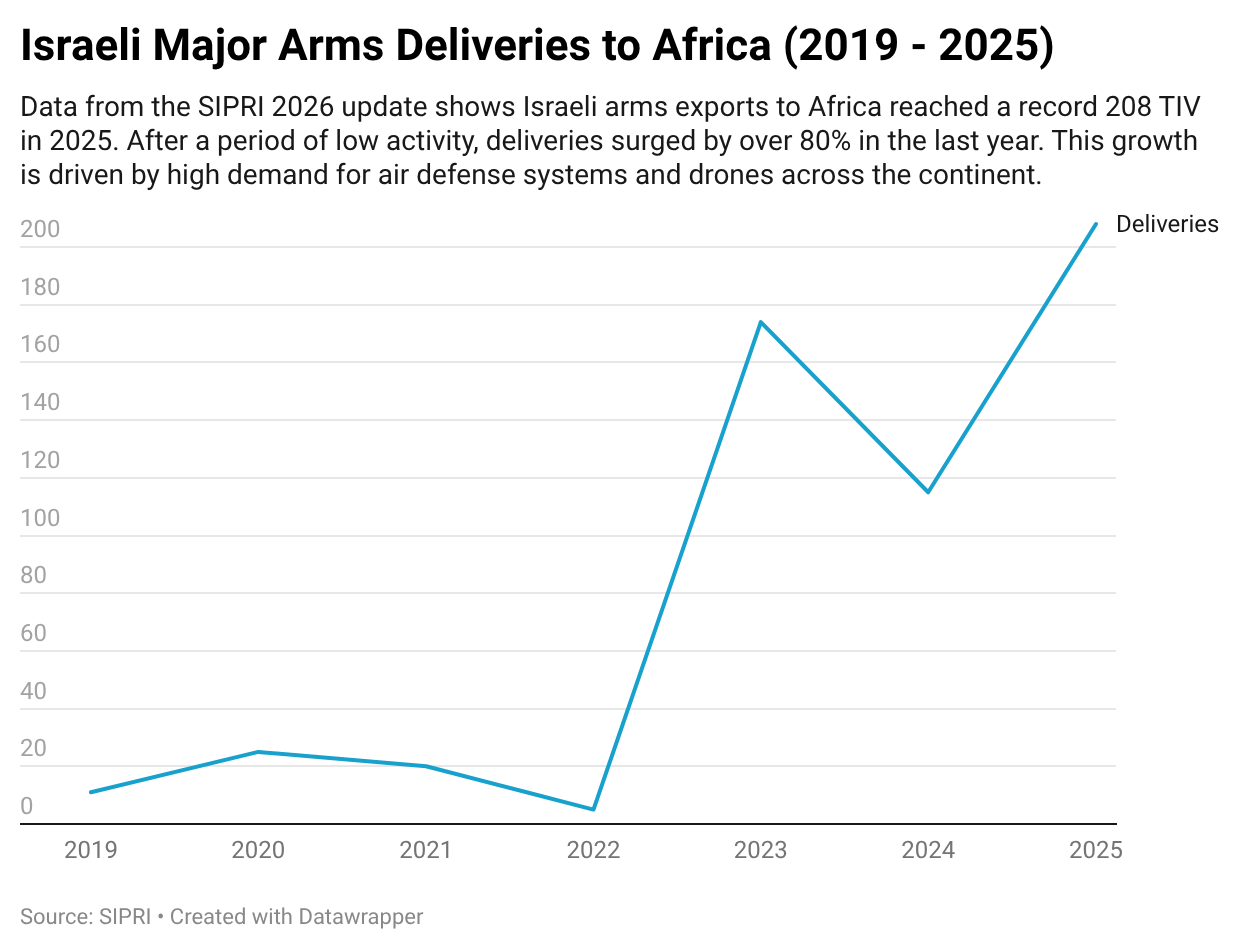

SIPRI data shows that Israeli deliveries of major arms to African countries rose to 174 in 2023, followed by 115 in 2024, and then climbed again to 208 in 2025. This shift stands well above historical levels and signals a clear change in activity.

At first glance, it’s easy to look at this as just another defense story, but the numbers alone do not explain what is actually happening. Arms transfers are early signals of something more durable. Once equipment enters a country, it creates long‑term technical and commercial dependencies that extend far beyond the initial sale.

This is where the real story begins. The increase in Israeli arms transfers is quietly building multi‑year service markets around maintenance, training, software, and system support. In other words, the data is only showing the starting point. The real value lies in everything that follows.

Why Are Israeli Arms Transfers to Africa Increasing Now?

The recent increase in Israeli arms transfers is closely tied to rising security demand across multiple African countries. Data from the Stockholm International Peace Research Institute shows that countries dealing with insurgency, terrorism, and border instability have continued to maintain or increase defense spending.

In countries like Nigeria, prolonged counterinsurgency operations have driven demand for surveillance systems and aerial monitoring technologies. According to ISS Africa, Nigeria’s military operations against Boko Haram and ISWAP rely heavily on intelligence and aerial surveillance capabilities. These are not short‑term needs, which means procurement tends to be sustained rather than occasional.

Nigeria has also acquired Israeli-origin surveillance and UAV systems over time, and their continued deployment in active operations creates ongoing demand for maintenance, training, and technical support, reinforcing the recurring nature of these systems

A similar pattern appears in Kenya, where border security operations linked to instability in Somalia have increased reliance on surveillance and monitoring systems. Data shows Kenya’s arms imports have shifted from being irregular to a period of rapid growth. After years of very low activity, procurement jumped to 71 units in 2020. This was followed by a record-breaking surge to 117 units in 2025 the highest level in over 25 years. This recent increase, led by the 2025 purchase of Israeli air defense systems, shows a clear trend of countries in East Africa upgrading their military technology.

What connects both countries is the continuous nature of those threats, which requires systems that can operate long-term.

At the same time, diplomatic shifts have expanded Israel’s access to African markets. Following normalization agreements in 2020, countries such as Morocco have deepened defense cooperation with Israel, opening the door for larger and more structured deals. This reduces political barriers and allows procurement relationships to scale more quickly.

Israeli defense firms are also positioned to meet these needs directly. Companies like Elbit Systems and Israel Aerospace Industries specialize in drones, surveillance platforms, and border security technologies systems that match the operational realities in many African countries.

When you put these pieces together, sustained security pressure, stable defense spending, improved diplomatic access, and matching supplier capabilities, the timing becomes clearer. The increase is the result of these factors aligning at the same time.

How Do Arms Transfers Translate Into Long‑Term Commercial Markets?

The commercial impact becomes clearer after deployment. These systems require continuous servicing, operator training, and technical support to remain operational, creating recurring demand tied directly to their use.

Take drones and UAVs as an example. Israeli firms such as Elbit Systems and Israel Aerospace Industries are among the leading UAV manufacturers globally. These systems require regular maintenance, replacement of key components, and continuous operator training to remain functional. In Nigeria, where UAVs are used in active military operations, their effectiveness depends on constant technical support and servicing. That ongoing need creates recurring service contracts tied directly to the equipment.

The same structure applies to surveillance and monitoring systems. Countries like Kenya deploy integrated monitoring technologies that depend on software updates, cybersecurity support, and system calibration. These require continuous engagement with the supplier or certified partners.

More advanced systems create even deeper dependency. Platforms developed by Rafael Advanced Defense Systems, including missile and air defense systems, operate within tightly controlled technical frameworks that require specialized maintenance and restricted access to spare parts. In countries like Morocco, where such systems are part of broader defense agreements, the complexity of the technology makes switching providers difficult after deployment.

Air defense platforms such as the SPYDER system provide a clear example of how this translates into revenue. These systems rely on integrated radar, command networks, and missile coordination, all of which require periodic upgrades, calibration, and trained operators. Servicing is typically handled by the original manufacturer or certified partners, creating recurring revenue streams linked to system uptime and operational readiness.

This is what drives the Maintenance, Repair, and Overhaul (MRO) market. Defense industry analysis shows that lifecycle servicing can account for a significant share of total system cost over time, often extending well beyond the initial purchase. What starts as a hardware sale evolves into a long-term service relationship.

So when you look back at the transfer data, it becomes clearer what it represents. It is the beginning of multi-year commercial ecosystems built around keeping that equipment operational.

Which African Countries Are Driving This Market and Why Do They Matter?

Morocco has emerged as a major recipient of Israeli defense systems in Africa, with publicly reported deals including surveillance satellites, drones, and radar platforms. Its defense relationship with Israel has expanded into long-term cooperation, including local industrial partnerships, making it a hub for the development of service ecosystems.

Nigeria has been one of the most consistent buyers of Israeli equipment in sub-Saharan Africa and remains a high-value recurring market due to its ongoing counterinsurgency and border operations, which require continuous support for drones, surveillance systems, and patrol technologies.

Kenya’s procurement of systems such as the SPYDER air defense platform demonstrates how structured engagement often comes with financing and long-term servicing arrangements, keeping supplier relationships active well beyond delivery. Smaller states like Rwanda and Cameroon also contribute to the ecosystem, with limited procurement generating ongoing demand for training, maintenance, and system upgrades. Even when the scale is lower, the commercial logic remains consistent, as all these countries represent entry points into long-term service economies built around the Israeli systems they operate.

Where Are the Real Commercial Opportunities for Investors?

The real opportunity sits in what happens after deployment. Once systems are in use, they generate continuous demand for servicing, upgrades, and operational support. Evidence from Israel–Africa defense relationships shows that contracts often include maintenance, training, and system upgrades as part of long-term cooperation frameworks. These services are required to keep systems operational, which makes them recurring and predictable.

In many cases, servicing is restricted to the original manufacturer or certified partners, limiting competition and creating controlled market access.

This creates a controlled market structure. In many cases, servicing can only be performed by the original manufacturer or certified partners. That limitation reduces competition and opens the door for local firms to enter as licensed partners, particularly in countries that support domestic participation.

In Nigeria, defense policy frameworks such as the Defence Industries Corporation of Nigeria (DICON) Act emphasize local participation and domestic capacity development, creating potential pathways for local firms to engage in maintenance, repair, and overhaul partnerships.

Across Africa, similar local content and offset requirements are increasingly shaping defense agreements, requiring foreign suppliers to engage local partners for servicing, training, and technical support.

Additional opportunities also appear in logistics, training, and technology services. Systems that rely on data, surveillance, and cybersecurity create demand that extends beyond defense into broader infrastructure and digital services.

At this point, the pattern is consistent with what we saw earlier. Arms transfers introduce the systems, but the long-term value is captured in the services that keep those systems running.

The key question is no longer who is selling the equipment, but who controls the servicing, training, and operational support value that follows.