Table of Contents

In Summary

- Cellulant began as a mobile content venture before switching into a continental payments platform serving over 35 African markets.

- The $47.5 million Series C led by The Rise Fund in 2018 remains one of Africa’s most significant fintech growth rounds.

- Cellulant secured regulatory approval to operate in Egypt in 2023, expanding its reach across North, West, East, and Southern Africa.

Deep Dive!!

Lagos, Nigeria, Tuesday, December 9 – Cellulant began operating in the early 2000s with a focus on mobile content services before transitioning into digital payments as African markets opened up to mobile banking and electronic transactions.

Under Ken Njoroge’s leadership, the company concentrated on building payment infrastructure that could serve banks, mobile-money operators, merchants and government institutions across multiple regions. This approach positioned Cellulant as one of the few African technology companies developing payment rails that function across numerous regulatory environments.

A major inflection point came in 2018 when the company secured a US$47.5 million Series C investment led by The Rise Fund. The round was one of the largest fintech growth raises in Africa at the time and enabled Cellulant to strengthen its enterprise technology, expand market operations and deepen integrations with financial institutions across the continent.

The company reports operations in more than 35 African markets. Its regulatory approval to operate in Egypt in 2023 marked further penetration into North Africa and added to its existing presence in West, East, Central and Southern Africa.

Cellulant’s presence reflects a long-term strategy built around infrastructure rather than consumer-facing products. The company’s continental footprint, institutional partnerships and enterprise integrations illustrate its role in shaping digital payment capabilities across multiple African economies.

Early Life, Education, and Experience

Public information about Ken Njoroge’s early personal life is limited, but what is documented is his long-standing involvement in technology, entrepreneurship, and product development in East Africa. Before co-founding Cellulant in 2003, he built and ran 3Mice Interactive Media, one of Kenya’s earliest web-development and digital-services companies.

Under his leadership, 3Mice grew into a respected regional digital agency serving corporate clients during the early rise of the internet on the continent. The company was later acquired by Africa Online, one of the leading internet providers in Africa at the time, marking Njoroge’s first major entrepreneurial exit.

Following the acquisition, Njoroge continued working within the African tech ecosystem, gaining hands-on experience in building digital products, managing teams, and delivering technology solutions across multiple markets. These roles exposed him to the operational gaps in digital infrastructure and payment systems insights that later proved essential in shaping Cellulant’s strategy.

By the early 2000s, with experience in product development, corporate technology services, and regional operations, Njoroge was well-positioned to build a company that could address Africa’s emerging digital payments challenges.

This combination of practical entrepreneurial experience and regional technology exposure laid the foundation for the creation and early direction of Cellulant.

Inspiration to Start Cellulant

The origins of Cellulant trace back to a conversation between its co‑founders, Ken Njoroge and Bolaji Akinboro. The two first sketched the initial business idea in 2002 reportedly on a serviette during a dinner meeting.

At the time, the plan was not to build a fintech infrastructure. As Bolaji Akinboro later admitted, “We set out originally to sell music through mobile phones.” Their initial business focused on mobile content like ringtones, music and news delivered via carrier networks.

But as they rolled out mobile‑content services, they ran into persistent challenges around payment handling. The billing systems of mobile carriers were expensive and inefficient, and their experience revealed a deeper structural problem such as payment infrastructure across African markets was weak, fragmented, and unreliable.

That tension between a growing demand for mobile services and inadequate payment systems pushed Njoroge and Akinboro to reconsider. As Njoroge explained, when banks and financial institutions initially balked at trusting mobile-based payments, those rejections only strengthened their conviction. “Banks would tell us, ‘Guys, get serious, who on earth would trust a financial transaction made from their phones?’” a question he recalled during a 2017 interview.

The turning point came with the early success of mobile‑money systems in Kenya, particularly M-Pesa. By the end of 2007, when M-Pesa had demonstrated that mobile payments could scale in Africa, Njoroge said: “The argument was settled.”

That validation convinced them to pivot fully from content to payments. The conviction was not only about business viability it was underpinned by a broader ambition to build an African company that could operate across the continent, solving payment infrastructure problems at scale. As Njoroge later reflected

“I do what I do because I am passionate about our dignity as Africans.”

He described Cellulant not simply as a business, but as a statement about what Africans can build with technology and vision. That sense of purpose aligning commercial success with continental transformation became a core inspiration behind Cellulant’s founding and early strategy.

What problem Cellulant solves

Across Africa, businesses and consumers face a fragmented payments landscape, with hundreds of mobile-money wallets, banks, card networks, and diverse payment methods that vary by country. Merchants operating in multiple markets often struggle to collect payments, reconcile transactions, handle refunds, and manage currency and regulatory differences.

Cellulant addresses these challenges by providing a unified pan-African payments infrastructure, enabling enterprises to accept payments efficiently across multiple countries and platforms while reducing operational complexity.

- Fragmented payment systems across countries and providers - Africa’s payments environment is highly decentralized, with separate networks for mobile money, bank transfers, and card payments in almost every country. Cellulant’s unified API allows businesses to process transactions from multiple providers through a single integration, reducing operational costs and enabling cross-border scalability. By 2025, the platform connects over 35 African countries and integrates with leading mobile-money operators, banks, and card networks.

- High friction for merchants - Merchants previously managed multiple devices, logins, and reconciliation processes for each payment provider, resulting in lost revenue, errors, and delays. Cellulant centralizes collections, settlement, and reporting, giving merchants a single dashboard and automated reconciliation tools. This reduces operational friction and enables enterprises to scale without proportional increases in administrative burden.

- Limited access for SMEs and underserved markets - The majority of African businesses are SMEs, many of which previously relied entirely on cash transactions due to inaccessible or costly digital payment solutions. Cellulant’s infrastructure allows these businesses to accept mobile-money payments, card payments, and bank transfers with minimal technical overhead. In Kenya alone, over 40,000 SMEs have integrated with Cellulant’s platforms, allowing them to operate digitally, track revenue, and expand customer reach.

- Low banking and card penetration - Debit and credit card penetration across Africa averages 3–5%, with many populations unbanked or underbanked. Cellulant extends financial inclusion by enabling payments via mobile wallets, local bank transfers, and other country-specific digital channels. This inclusive approach allows businesses to access previously untapped customer segments and reduces reliance on cash transactions, which carry higher risk and operational costs.

- Cross-border and multi-currency complexity - Enterprises operating across African markets face regulatory variation, currency conversion issues, and delayed settlement cycles. Cellulant provides cross-border payment solutions, automating currency conversion and adhering to local compliance requirements, thereby reducing settlement delays from days to near real-time in some markets. By 2025, the platform supports transactions across West, East, Southern, and North Africa.

- Reconciliation and back-office inefficiencies - Previously, businesses had to manually reconcile payments from multiple sources, resulting in errors, delayed reporting, and poor cash-flow management. Cellulant offers automated reconciliation, integrated reporting dashboards, and payout management, enabling businesses to process large transaction volumes efficiently. This operational efficiency has been critical for enterprises handling hundreds of thousands of daily transactions, such as utility companies and e-commerce platforms.

By solving these structural and operational challenges, Cellulant reduces barriers to digital commerce, supports cross-border trade, and creates a more inclusive and reliable payments ecosystem for businesses and consumers across Africa. Its unified infrastructure has positioned the company as a backbone for digital transactions across the continent, enabling economic participation for previously underserved populations.

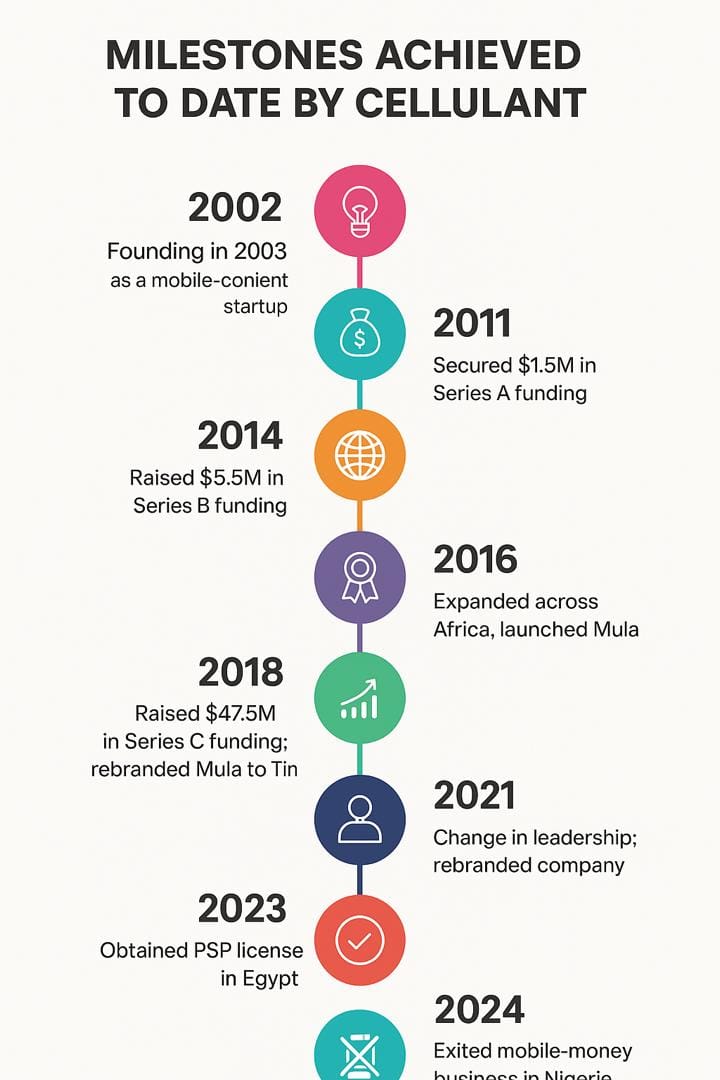

Milestones Achieved to Date by Cellulant

Cellulant’s journey from a mobile‑content startup to a pan‑African payments infrastructure provider is marked by multiple significant milestones like funding rounds, platform evolution, continental expansion, regulatory licensing, rebranding, and scale metrics. Below is a chronological and thematic summary of the key milestones.

Cellulant traces its origin to 2002, when its founders sketched the first business idea on a serviette. The company was formally founded in 2003, initially focusing on mobile content like selling ringtones, music, and other carrier‑based content to users across East and West Africa. Early operations included launches in markets like Uganda (via Uganda Telecom), Ghana (with Spacefon), and Nigeria (via a joint venture with a local partner). Through this mobile content business, Cellulant reportedly reached around 8 million consumers, establishing an early user base.

As mobile content services revealed payment inefficiencies (especially in carrier‑billing), the founders began to re-think their business model. Over time they pivoted from content delivery toward payment infrastructure connecting banks, mobile‑money operators, merchants, and end-users.

In 2011, Cellulant secured its first institutional funding: a Series A round of US$1.5 million from TBL Mirror Fund. This investment helped the company begin to build a converged payments ecosystem linking banks, merchants, mobile networks and consumers.

Three years later, in February 2014, the company raised US$5.5 million in a Series B round led by Velocity Capital FinTech Ventures. This funding supported the shift from mobile banking/wallet offerings into a more complete stack of mobile payments services across multiple African countries.

By 2016, Cellulant had expanded its pan‑African reach significantly. By that time it operated in multiple African markets by 2016 the company’s payment network reportedly connected over 50 banks and more than 40 mobile‑money operators, and reached roughly 40 million end users. In 2016 the company won “Best Payments and Transfer Company Africa” at the African FinTech 100 Awards, a continental recognition of its growing influence.

Cellulant then launched a mobile‑money/wallet application under the brand Mula, targeting consumers directly. The platform expanded across several countries including Kenya, Uganda, Tanzania, Ghana and others. Alongside Mula, the company began building an on‑the-ground agent network to extend payment reach to offline users, a strategic move to capture both digital and physical‑world payment demand.

In May 2018 the company raised a landmark US$47.5 million in a Series C funding round led by The Rise Fund (TPG Growth’s impact‑investment arm), with participation from Satya Capital, Endeavor Catalyst, Velocity Capital and Progression Africa. At the time, this was the largest funding round for an African fintech operating solely on the continent. The investment provided capital for expansion, infrastructure scaling, and deeper market penetration across Africa.

By 2018, with the boost from the Series C, Cellulant’s payment platform was live in 11 African countries. The company reported serving about 40 million users and working with over 120 financial partners (banks, mobile money operators and other payment providers). Key markets included Kenya, Nigeria, Zambia, Ghana, Zimbabwe, Tanzania, Uganda, Botswana, Mozambique, Malawi and Liberia.

In 2019 Cellulant rebranded its consumer‑facing app Mula into Tingg repositioning as a unified payments “super‑app” and integrating services like bill payments, merchant payments, lending, group investments, and e‑commerce across multiple African markets. This marked a strategic shift from a loosely connected set of mobile services toward a unified payments infrastructure for both consumers and enterprises.

2021 marked a major leadership and organizational transition. After 18 years at the helm, co-founder and long‑time CEO stepped down, and the company reorganized under what Cellulant termed “Cellulant 3.0.” Acting CEO (previously CFO) was confirmed as Group CEO on October 1, 2021. This transition accompanied a refreshed brand identity and a renewed focus on making Tingg (the payments platform) the core product across all markets.

Beyond management changes, Cellulant continued building its enterprise infrastructure. The platform scales to support a wide variety of sectors such as the airlines, telecoms, retail, e‑commerce, ride‑hailing, utilities, and remittances. By 2022, the company claimed presence in 35 African countries and maintained physical offices in roughly 18–19 of those, a sign of deep continental penetration.

A further regulatory milestone came in November 2023, when Cellulant obtained its first Payment Service Provider (PSP) and Payment Facilitator licence in Egypt. This made Egypt the newest country in its footprint and extended Cellulant’s reach into North Africa. The licence broadened its ability to offer collections, disbursements, online and offline payments for both regional and global merchants operating in Egypt.

As of that announcement, Cellulant claimed to integrate more than 370 payment methods, process payments across 35 markets, and maintain physical operations in 19 countries. According to the same report, it serves over 2,000 businesses and processes an estimated 20 million transactions monthly, collectively valued at about US$1 billion.

In 2024, the company announced exit from the mobile‑money business in Nigeria after surrender of its mobile‑money licence, following strategic repositioning. The firm said its shift away from mobile‑money operations began as early as 2021, aligning with a broader focus on enterprise payment solutions under its PSSP (Payment Solution Service Provider) licence, which it renewed in February 2023.

Throughout these milestones, Cellulant has evolved significantly from a mobile‑content provider to a full‑fledged payments infrastructure company serving thousands of enterprises and processing millions of transactions across the continent.

Lessons for Other African Entrepreneurs

Cellulant’s journey provides valuable insights for African entrepreneurs aiming to build scalable, continent-wide ventures. Its evolution from a small mobile-content startup to a pan-African payments infrastructure company highlights practical lessons in strategic decision-making, technology, partnerships, and resilience.

- Adapt business models to real market needs - Cellulant began as a mobile-content provider but pivoted to payments infrastructure after identifying structural gaps in Africa’s financial ecosystem. This shift allowed the company to address fragmented payment systems, low banking penetration, and operational inefficiencies, turning a localized service into a continent-wide platform.

- Leverage strategic fundraising - Across Series A, B, and C rounds, including the landmark US$47.5 million Series C in 2018 led by TPG Growth’s Rise Fund, Cellulant demonstrated the importance of raising capital aligned with long-term vision. Funds were directed toward building scalable technology, expanding regional presence, and establishing physical agent networks, directly supporting operational growth.

- Invest in proprietary technology infrastructure - Rather than relying on third-party systems, Cellulant built a robust API and platform connecting banks, mobile-money operators, and merchants across 35 African countries. Its infrastructure handles over 370 payment methods, supports multi-currency transactions, and automates reconciliation, enabling both enterprise and consumer adoption at scale.

- To build strong partnerships and ecosystem networks - Cellulant’s growth relied on integrating multiple stakeholders: banks, mobile money operators, telecoms, and merchants. These partnerships created network effects that increased adoption, operational efficiency, and trust across jurisdictions, illustrating the value of strategic collaboration in multi-country ventures.

- Focus on regulatory compliance and local adaptation - Expanding across African markets requires navigating diverse regulatory frameworks. Cellulant obtained necessary licenses, including PSP and Payment Facilitator licenses in Egypt (2023), ensuring compliance while scaling its services across different legal and financial environments. Adapting solutions to local market requirements was critical to sustainable growth.

- Maintain resilience and long-term strategic vision - Operating in fragmented African markets presents constant challenges: infrastructure gaps, competition, and regulatory changes. Cellulant’s ability to stay focused on its mission, invest in infrastructure, and gradually expand geographically demonstrates the importance of resilience and patience in building sustainable, pan-African enterprises.

By following these lessons, African entrepreneurs can better understand complex markets, design solutions for real structural challenges, and build ventures capable of scaling across the continent. Cellulant’s journey illustrates how strategy, technology, partnerships, and resilience combine to create lasting impact.

Cellulant’s journey demonstrates how strategic execution, robust technology, and cross-border partnerships can address structural gaps in financial systems. The company has systematically tackled low banking penetration, fragmented payments, and transactional inefficiencies while building scalable solutions for enterprises and consumers. Moving forward, Cellulant plans to expand regional coverage, deepen enterprise payment services, and integrate additional payment methods, providing a model for other African fintechs and reinforcing the continent’s digital financial ecosystem.

{kind=link}