Table of Contents

In Summary

- Ashraf Sabry founded Fawry in 2008, taking it from a bill-payment startup to Egypt’s first tech "Unicorn" listed on the Egyptian Exchange (EGX).

- The platform connects over 36 banks, 330,000 agents, and 50 million customers, processing hundreds of billions of Egyptian pounds in annualized total payment volume.

- Rather than just a mobile wallet, Sabry built a payment structure that allows unbanked Egyptians to pay for everything including government fines and insurance at their local grocery store.

- Under his leadership, Fawry has expanded its footprint into the UAE and is currently positioning itself as a primary payment bridge between North Africa and the Levant.

- Sabry’s 20-year background at IBM and Raya allowed him to build a system so robust that it now handles the vast majority of electronic bill payments in Egypt.

Deep Dive!!

Lagos, Nigeria, Saturday, December 27, 2025 - In 2008, Egypt was a nation defined by "the queue." To pay a phone bill, an electricity charge, or a government fee, a citizen had to physically travel to a specific office during limited hours and wait in line with a stack of cash. In a country of nearly 100 million people, this inefficiency was a massive drag on the economy. Digital banking was a luxury for the elite, leaving the vast majority of the population financially stranded.

Ashraf Sabry saw this not as a banking problem, but as a distribution and trust problem. He realized that Egyptians didn't need fancy apps but needed a way to digitize their cash at the nearest street-corner kiosk. He quit his high-flying corporate career to build Fawry not as a bank, but as a "layer" that sits between the consumer, the merchant, and the financial institution.

Today, Fawry is the "invisible utility" of Egypt. It is so deeply integrated into daily life that "Fawry it" has become a verb for making a payment. By combining high-tech backend rails with a "low-tech" network of neighborhood retailers, Sabry built the digital financial sovereignty of North Africa’s most populous nation.

Early Life, Education, and Experience

Ashraf Sabry’s path is a case study in how deep corporate rigor can be weaponized to solve systemic national problems. Unlike many startup founders who begin their ventures in their twenties, Sabry’s journey was built on two decades of elite-level experience within the global and regional technology sectors. He was born and raised in Egypt, where he pursued his foundational education at Cairo University, graduating with a Bachelor’s degree in Civil Engineering. This engineering background provided the structural and logical mindset necessary for systems thinking, but it was his subsequent move into the business and technology realms that defined his professional DNA.

To bridge the gap between engineering and global commerce, Sabry moved to the United Kingdom to earn a Master of Business Administration (MBA) from the University of Leeds, a move that equipped him with the financial and strategic tools to navigate multinational corporate environments.

His professional career began at IBM Egypt, where he spent a formative decade. During his ten years at IBM, Sabry rose to the position of Vice President of Sales, a role that gave him an intimate view of the digital infrastructure or lack thereof powering Egypt’s largest institutions. At IBM, he was selling the concept of digital modernization to a country that was still largely analog. This period was followed by another ten-year tenure at Raya Holding, one of Egypt’s most prominent ICT conglomerates.

At Raya, Sabry served as CEO, overseeing operations, finance, and business development. Under his leadership, Raya solidified its standing as a technology leader in the Middle East, and it was here that Sabry honed his ability to scale a business across borders, specifically within the regional North African and Gulf markets.

By 2008, Sabry had reached the pinnacle of the Egyptian corporate world, but he observed a persistent gap that neither the banks nor the tech giants were addressing: the "last mile" of financial services. Despite his seniority and the financial security of his role at Raya, he chose a path of radical risk. He left his corporate position to found Fawry, committing a significant portion of his personal savings to the venture.

This transition was particularly notable because it occurred during a period when the term "fintech" barely existed in the African lexicon and venture capital was virtually non-existent in Egypt. His decision to pivot from a corporate executive to a founder was driven by the conviction that his 20 years of experience at IBM and Raya had given him the unique technical blueprint required to engineer a national payment rail that could bypass the traditional, exclusionary banking system.

Inspiration to start Fawry

The catalyst for Fawry was Ashraf Sabry’s observation of the "time tax" that physical cash imposed on the Egyptian citizenry. In 2008, Egypt was a country of nearly 80 million people where fewer than 10% had a bank account. For the vast majority, the simple act of paying an electricity bill or a phone charge involved a grueling ritual of taking time off work, traveling to a specific government or corporate office, and standing in long, disorganized queues for hours. Sabry realized that while the banking sector was focused on high-net-worth individuals, the mass market was being ignored. His inspiration came from a desire to "democratize" the payment process by turning every local grocery store and pharmacy into a mini-bank branch, effectively decentralizing the country's financial infrastructure.

Sabry’s conviction was further fueled by his experience at Raya, where he saw the limitations of traditional ICT solutions in reaching the average Egyptian on the street. He understood that the problem wasn't a lack of desire for digital services, but a lack of proximity and trust. He envisioned a system that worked "with" the people's existing habits which revolved around the neighborhood "Baqal" (grocer) rather than trying to force them into a formal banking hall. This realization led to the conceptualization of an electronic bill presentment and payment (EBPP) platform that would act as a neutral bridge between the billers (telecoms, utilities, government) and the unbanked consumer.

The leap into entrepreneurship was a calculated but extreme risk. At nearly 50 years old, Sabry resigned from his stable, high-profile role as CEO of Raya to start Fawry from scratch. To secure the initial funding, he had to navigate a landscape where most investors viewed a cashless Egypt as a fantasy. He successfully pitched a consortium of local and international investors, including EFG Hermes and the IFC, by demonstrating that Fawry would solve a logistics problem, not just a financial one. He famously committed a large portion of his own savings to the seed round to prove his "skin in the game," emphasizing that he wasn't just building an app, but a national utility that would become as essential as the power lines themselves.

What problem Fawry solves

Fawry was built to overcome the "trust and distance" barriers that kept Egypt’s economy anchored to physical currency. Before its inception, the friction of cash transactions led to massive delays in revenue collection for the government and private sector alike. Sabry’s infrastructure created a unified digital network that allowed for the instant movement of value across a geographically dispersed and technologically diverse population.

1. Elimination of the "Queue Culture": Fawry’s primary achievement was the decentralization of payment points. By integrating with over 330,000 retail locations, it saved millions of Egyptians the hours previously lost in physical queues at utility offices and government bureaus.

2. Bridging the Banking Gap: For the 90% of Egyptians who were unbanked in 2008, digital finance was inaccessible. Fawry solved this by allowing cash-in/cash-out services at local kiosks, enabling users to pay digital bills with physical cash, effectively acting as a gateway to the formal economy.

3. Streamlining Government Revenue Collection: The Egyptian government struggled with slow and leak-prone manual collection systems. Fawry provided a secure, real-time "sovereign rail" for taxes, traffic fines, and license renewals, increasing transparency and the speed of national treasury inflows.

4. Interoperability Between Banks: Similar to the "switch" model, Fawry allowed Egypt’s fragmented banking sector to communicate. It provided the rails for 36 different banks to offer bill payment services to their customers through a single, aggregated interface.

5. Operational Efficiency for SMEs: Small businesses in Egypt often lacked the tools to accept electronic payments or manage credit. Fawry’s "Fawry Plus" and merchant tools provided SMEs with the digital infrastructure to accept cards and mobile wallets, expanding their customer base.

6. Reliability in a Low-Connectivity Market: Sabry built a system robust enough to operate in areas with inconsistent internet. By using a combination of POS terminals and USSD technology, Fawry ensured that a transaction in rural Upper Egypt was as reliable as one in central Cairo.

7. Consolidation of Fragmented Billers: Before Fawry, every utility and service provider had its own siloed payment system. Fawry acted as a master aggregator, bringing thousands of billers under one roof and providing a "one-stop shop" for the Egyptian consumer's financial life.

The systemic resolution of these problems turned Fawry into a national icon. By treating payment infrastructure as a public utility, Sabry provided the plumbing that allowed Egypt’s digital economy to flow. This model proved so successful that it served as the blueprint for Egypt’s rapid acceleration into a regional fintech hub, showing that infrastructure is the prerequisite for all other forms of digital innovation.

Milestones achieved to-date

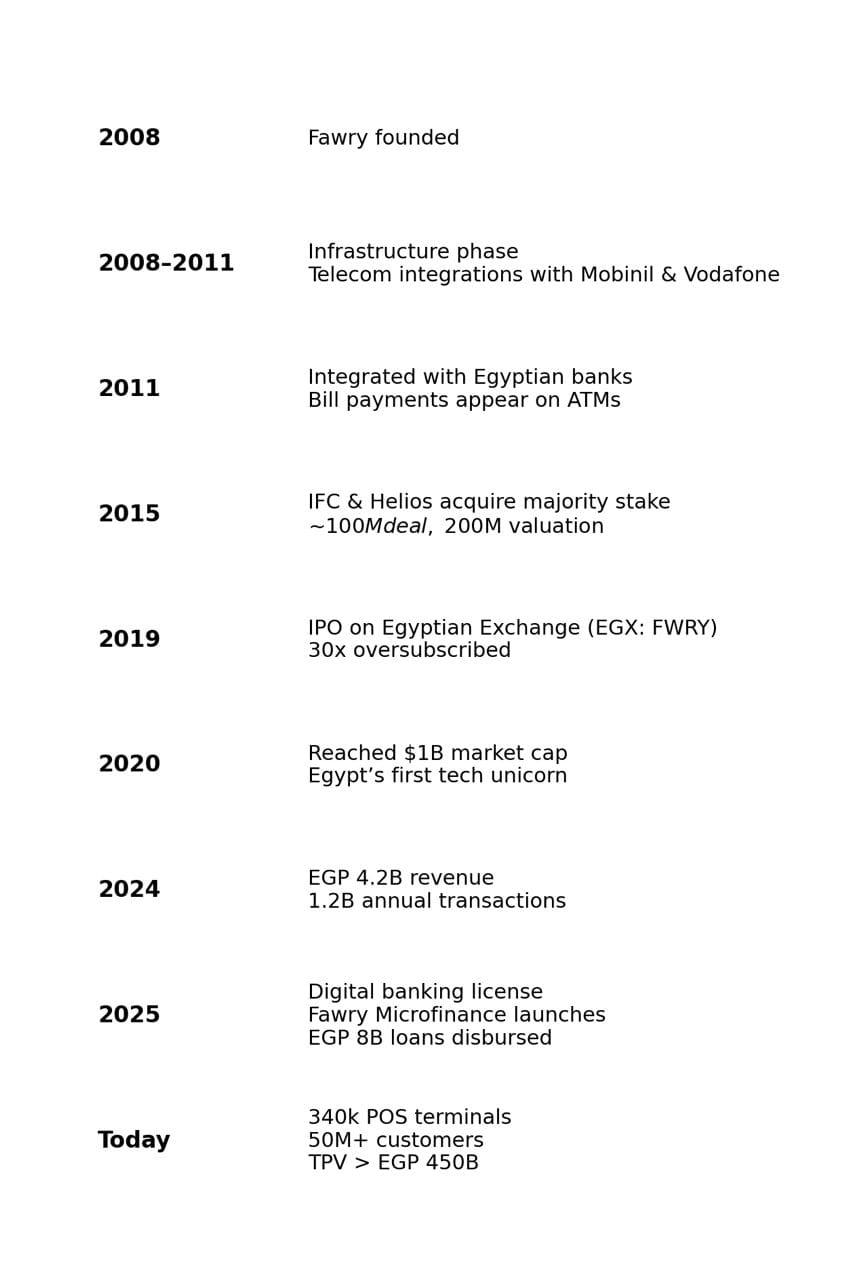

The history of Fawry is a record of consistent infrastructure layering, moving from the street-corner kiosk to the Egyptian Stock Exchange. Following its 2008 establishment, the company spent its first three years focusing on the "plumbing" signing the first critical contracts with telecom giants Mobinil and Vodafone Egypt to digitize airtime recharges. By 2011, Fawry achieved a fundamental breakthrough by integrating with the Egyptian banking sector, allowing its bill-payment services to appear on the ATMs of major national banks. This was the first time in North Africa that a third-party fintech became the "switch" for traditional banking institutions.

The mid-career phase of the company was marked by rapid scaling and institutional validation. In 2015, a landmark deal saw a consortium of international investors, including the International Finance Corporation (IFC) and Helios Investment Partners, acquire a majority stake for approximately $100 million, valuing the company at roughly $200 million just seven years after launch. This capital injection allowed Sabry to launch FawryPay and myFawry, transitioning the brand from a merchant-facing terminal to a direct-to-consumer digital wallet. In 2019, Fawry made history by listing on the Egyptian Exchange (EGX: FWRY); the IPO was oversubscribed by 30 times, and by 2020, Fawry became Egypt’s first tech company to reach a $1 billion market capitalization, officially becoming the nation’s first "Unicorn."

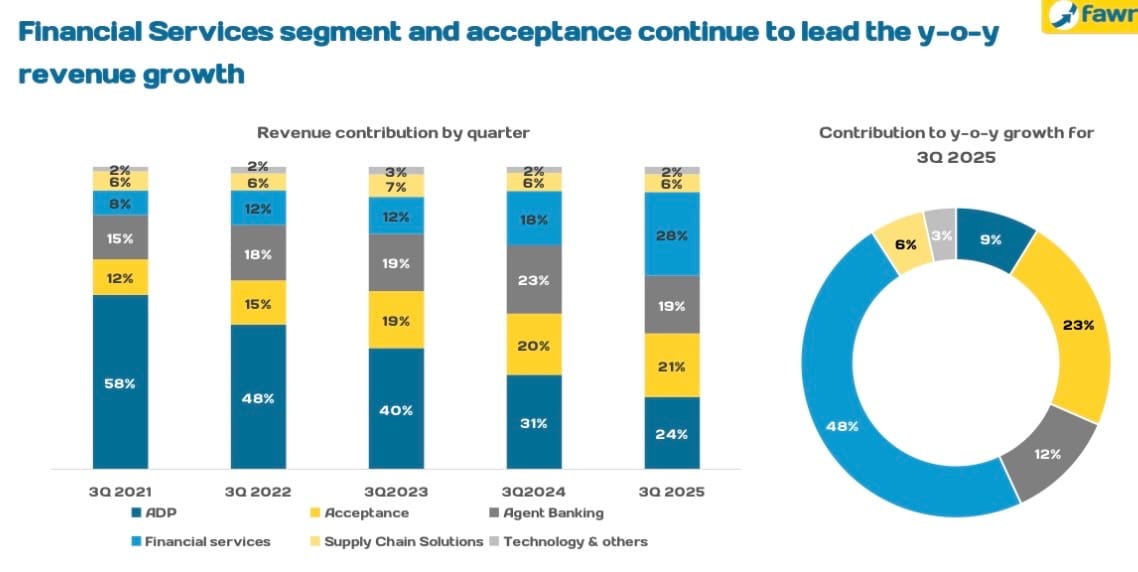

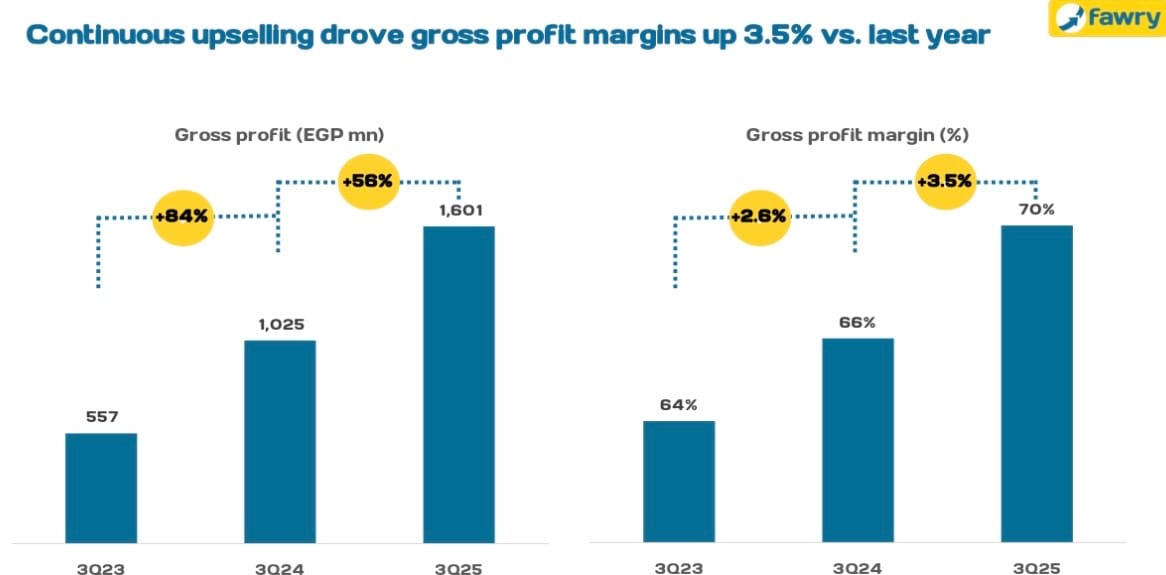

As of December 2025, the data reflects a massive industrial ecosystem. For the fiscal year ending 2024, Fawry reported an unprecedented EGP 4.2 billion in revenue, driven by a transaction volume of over 1.2 billion processed requests annually. The network now commands over 340,000 POS terminals and serves more than 50 million unique customers across Egypt.

A critical pivot occurred in late 2024 and early 2025 as the company moved into "Banking-as-a-Service," securing a digital banking license from the Central Bank of Egypt and launching Fawry Microfinance, which has already disbursed over EGP 8 billion in loans to small merchants.

Today, Fawry is a diversified financial engine operating across Egypt and the UAE, processing an annualized Total Payment Volume (TPV) exceeding EGP 450 billion.

Lessons for other entrepreneurs

The path of Ashraf Sabry serves as a corrective to the "youth-centric" and "asset-light" narratives of modern Silicon Valley. His ability to build a dominant, systemic institution in a complex regulatory environment like Egypt provides a strategic playbook for founders aiming for deep industrial impact. Sabry’s success is rooted in the belief that technology in Africa must be inclusive, visible, and deeply integrated into the existing social fabric.

1. Maturity is a Competitive Advantage: Sabry started Fawry at nearly 50 years old with 20 years of experience at IBM and Raya. He argues that "entrepreneurial spirit is more important than age" and that deep corporate experience provides the discipline and institutional memory required to build infrastructure that lasts.

2. Solve for "Trust" before "Technology": Egyptians didn't initially trust digital apps, but they trusted their local grocers. Sabry’s "phygital" model placing POS terminals in neighborhood kiosks allowed users to digitize cash in a familiar environment, proving that solving the "trust gap" is the prerequisite for digital adoption.

3. Monetize Through Recurring B2B Services: Rather than relying solely on consumer transaction fees, Sabry pivoted Fawry’s revenue mix toward banking services, ERP tools for SMEs (Fawry Business), and insurance. Today, over two-thirds of Fawry’s revenue is generated from these high-margin, recurring B2B operations.

4. Skin in the Game is the Best Pitch: To convince skeptical early investors, Sabry committed 80% of his personal savings to Fawry. He demonstrated that for a founder to lead a national-scale project, they must be willing to bear the primary financial risk, which in turn signals ultimate confidence to institutional partners.

5. Persistence through "Near-Bankruptcy": Sabry often recounts being nearly bankrupt three years into the journey. His lesson is simple: "never give up and be persistent." Infrastructure takes longer to build than software, and the reward of the "moat" only becomes visible 5 to 10 years into the business.

6. Institutionalize Early: Unlike founders who avoid institutional shareholders to maintain control, Sabry welcomed partners like the IFC and Helios early on. He believes that having institutional weight behind a startup is critical when dealing with regulators and the large-scale banking systems necessary for a national switch.

7. Dominate the "Last Mile": Fawry’s "Secret Sauce" was not its code, but its distribution. By creating a female-led agent network (Heya Fawry) and targeting rural Upper Egypt, Sabry ensured that his brand became a daily necessity for the unbanked, creating a defensive barrier that global competitors cannot easily replicate.

Ashraf Sabry’s legacy is the transformation of Egypt from a "queue-based" society into a digital-first economy. As of December 2025, the focus has shifted from simple bill payments to becoming a comprehensive Financial Super App. Looking forward to 2026, Fawry is aggressively pursuing its "Regional Champion" strategy, leveraging its new digital banking license to expand into micro-lending and Shariah-complaint savings and investment products. By establishing a holding company to manage regional acquisitions in Saudi Arabia and Iraq, Sabry is ensuring that the Fawry "rail" becomes the standard for the entire MENA region. His journey proves that when an engineer-turned-CEO commits to solving a fundamental social friction, the result is not just a company, but a sovereign digital asset that empowers a nation.

{kind=link}