Table of Contents

The question of whether Uganda will achieve first oil is settled. The more important question is who will capture the margins around it. The sector has decisively shifted from exploration into execution, and activity is surging across roads, wells, processing facilities, pipelines, and the services that support them, that is, logistics, insurance, project finance.

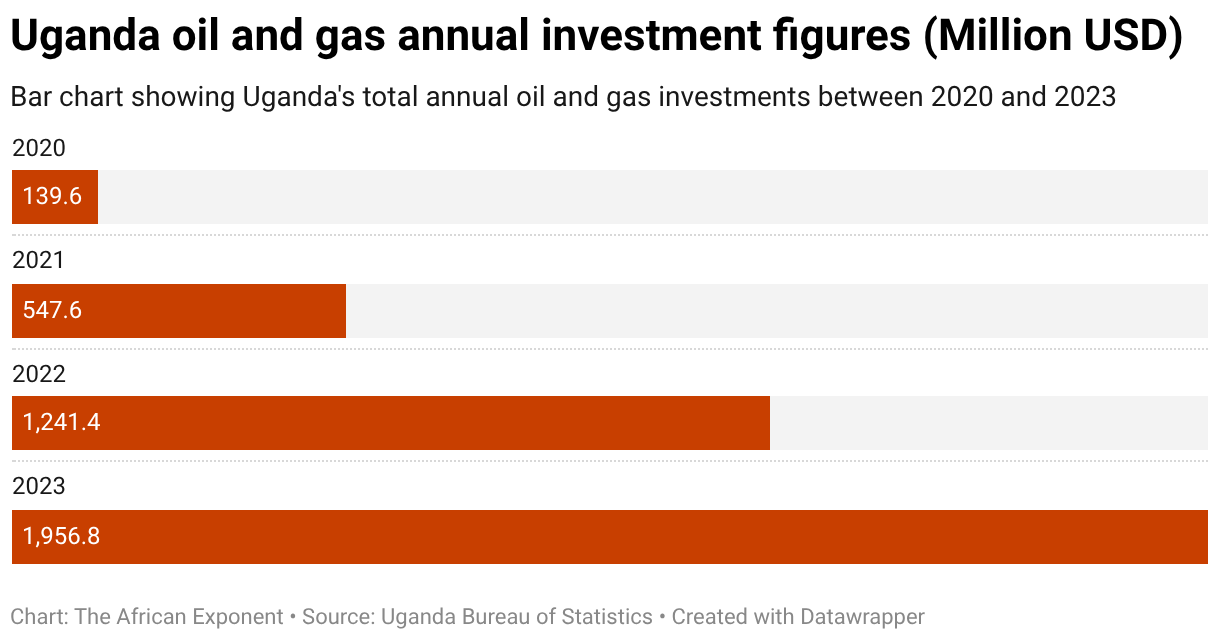

Data from the Uganda Bureau of Statistics shows how steep the climb has been: oil and gas investment rose from $139.6 million in 2020 to $547.6 million in 2021, $1.24 billion in 2022, and $1.96 billion in 2023. Crucially, 99.9% of 2023 spending went to development rather than exploration. Uganda's petroleum sector is no longer a speculative promise; it is an industrial operation. Capital is no longer circling the resource bit is building the pipelines, plants, wells, and logistics chains around it.

The execution phase is reshaping capital flows well beyond the oil patch, pulling investment into transport, logistics, insurance, and professional services. According to the Uganda Investment Authority, foreign direct investment reached $2.99 billion in 2023 and $3.30 billion in 2024, growth driven largely by petroleum developments. Uganda's oil is becoming more than an export commodity; it is the primary engine of capital allocation across the economy.

How is the oil boom redefining Uganda's broader investment map?

Oil is actively redrawing Uganda's investment map. Data from the Bank of Uganda, the Uganda Investment Authority and UBOS shows that oil and gas projects, namely Tilenga, Kingfisher and the East African Crude Oil Pipeline, attracted 62.4% of the country's foreign direct investment in 2022. By 2023 that concentration had deepened, with 97.4% of FDI inflows linked to oil sector activity. When that much capital flows into a single value chain, the real opportunity is no longer at the drill pad. It is in the services and infrastructure supporting the entire sector.

In March 2025, Reuters reported that EACOP had secured its first tranche of external financing. The pipeline anchors a wider $15 billion energy initiative led by TotalEnergies, CNOOC and their partners. Budgeted at $5 billion, though independent estimates now put costs closer to $5.6 billion, the project stretches 1,443 kilometres from Uganda to Tanzania, 296 of them on Ugandan soil and 1,147 in Tanzania. It is more than infrastructure. It is a long-term economic engine generating sustained demand for banking, procurement, freight, legal and risk management services.

Oil investment is also powering the upstream infrastructure needed to get the resource out of the ground. According to EACOP's official overview, the Kingfisher project features a central processing facility capable of handling 42,000 barrels per day, while Tilenga operates 31 wellpads and a 204,000-barrel-per-day processing facility. Uganda's planned refinery holds first rights to 60,000 barrels per day, leaving the rest for export. These operations do more than lift oil volumes. They expand the entire industrial value chain, and they pose a strategic question for local business. Beyond the crude itself, how much of this growing support ecosystem can Ugandan firms capture?

Insurance shows how far the frontier has moved. At the 2025 ICOGU Energy Symposium in Kampala, the Petroleum Authority of Uganda noted that 36 insurance companies are now registered on its National Supplier Database, with 13 actively serving the sector. Projects require coverage for pipeline operations, marine cargo and storage infrastructure, and the insurance regulator is rolling out an ESG framework for the industry. Every major project generates its own market for risk transfer, well past the drill sites.

Why do Ugandan firms capture a small share of the total oil contract value?

At first glance, local-contract figures look promising, but the real story lies in the value split. Data from the Uganda Bureau of Statistics shows that in 2022, Ugandan firms won 820 of the 930 contracts awarded, an 88.2% share. Yet those contracts were worth only $579.98 million of the $3.29 billion total, just 17.6% of value.

The 2023 numbers require careful reading. Ugandan companies won 720 of 852 contracts (84.5%) worth $257.8 million, and their share of value jumped to 51.4%. That looks like progress. It isn't. Total contract value collapsed to $501 million as the mega packages of 2022 worked through the system, and local firms' absolute earnings fell by more than half. The share rose because foreign-awarded value shrank, not because Ugandan firms climbed the value chain. The pattern is consistent across both years. Local participation is broad, but when the capital-intensive, technically complex work is on the table, the money flows elsewhere.

This turns Uganda's first-oil economy into a supplier-finance challenge. A company can hold every registration and certification and still miss lucrative work because it lacks working capital, performance guarantees, specialised equipment or insurance backing. The market gap is not "more contracts." It is financing and upgrading local players so they can bid for larger, riskier and more technical projects. The next commercial opportunity lies in helping local firms move from simple subcontracting to the balance-sheet strength and prime-contract readiness needed to compete at the top.

Where are the highest-growth opportunities in Uganda's evolving oil execution layer?

The best opportunities now sit in the execution layer, the services that actually make the oil flow. That means industrial logistics, equipment leasing, warehousing, fabrication and workforce housing, alongside specialised support such as HSE compliance, training, marine and cargo insurance, reinsurance and EPC subcontracting.

Crucially, it also means better supplier finance. Providers offering invoice discounting, contract-backed lending and tailored working-capital products will turn contract wins into delivered work.

Meanwhile, project milestones signal that the window is narrowing. The Petroleum Authority of Uganda reported in late 2025 that Kingfisher had drilled 15 of the 17 wells required for production, and by October the central processing facility stood at 93% complete with the well threshold met. Tilenga has passed its first-oil drilling requirements, and reports from early 2026 put the export pipeline at 80% complete, with first exports expected around October 2026, dependent on the readiness of storage, pump stations and the marine terminal. Whatever the exact date, the message is the same. The commercial upside sits not in the crude itself but in the network that delivers it to market.

Ultimately, Uganda's oil boom runs on supplier capacity, not just production. The winners won't merely hold reserves or pipeline shares. They will be the firms, local and foreign, that clear the hurdles between winning a contract and delivering the work, and that help Ugandan suppliers shift from winning contracts to capturing project value. Smart money already understands this. It is backing those who turn potential into performance.