Table of Contents

For much of the past decade, Africa’s currency narrative has been dominated by crisis. Inflation surges, widening fiscal deficits, and repeated devaluations in major economies such as Nigeria, South Africa, and Egypt shaped perceptions of persistent foreign exchange fragility across the continent. Yet beneath this dominant storyline, a quieter and more instructive trend emerged. From 2025 into 2026, Africa’s strongest year-to-year currency performance did not come from its largest economies or most politically prominent reformers. It came from smaller, less volatile countries that treated monetary stability as an essential policy objective rather than a political tool.

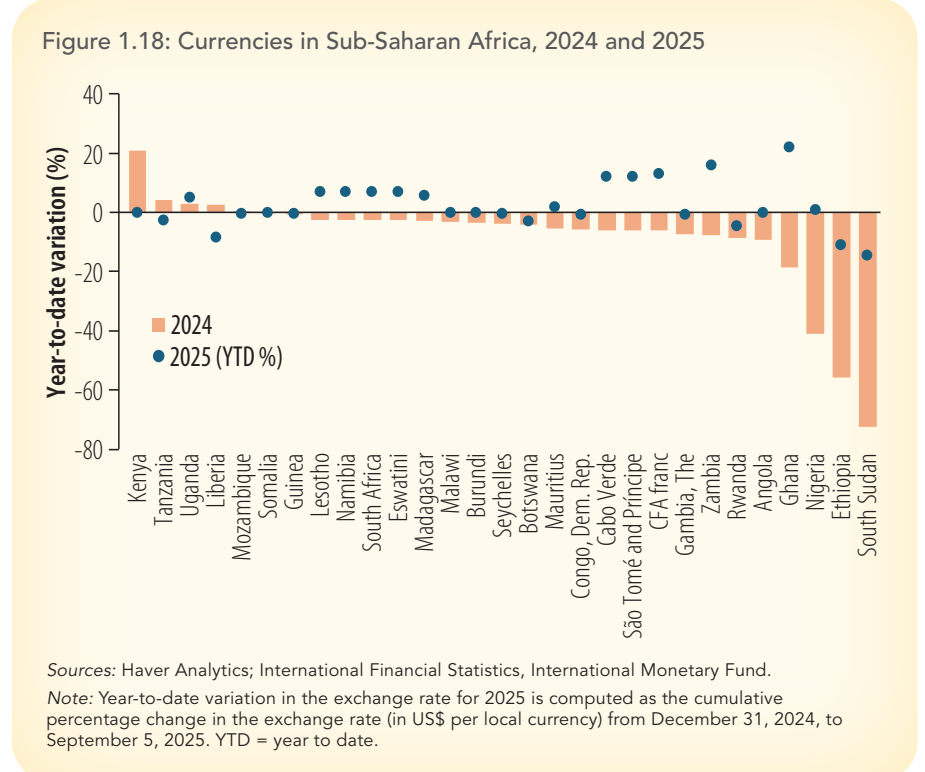

Data from the October 2025 edition of Africa’s Pulse reports published by the World Bank Bank show that currencies such as Ghana’s Cedi and Zambia’s Kwacha recorded some of the strongest gains against the US Dollar. These outcomes reflected disciplined monetary policy, tighter fiscal coordination, stronger export earnings, and deliberate foreign exchange management. While larger economies struggled with economic imbalances due to highly politicized market policies and volatile capital flows, smaller and mid-sized countries demonstrated that policy clarity and credibility often mattered more than perceived economic strength.

How did Ghana’s Cedi and Zambia’s Kwacha Outperform Africa’s Currency and Economic Giants?

Ghana’s Cedi delivered one of the most striking currency reversals on the continent in 2025. After years of depreciation, the currency appreciated by more than 20 percent against the US dollar, making it Africa’s best-performing currency. This turnaround was driven by a commodity boost and a coordinated policy reset combining fiscal restraint, and higher interest rates.

According to a report by the Governor of the Bank of Ghana, Dr. Johnson Asiama, Ghana’s foreign exchange reserves rose to nearly $14 billion by the end of 2025, strengthening the Bank of Ghana’s ability to manage currency volatility and meet external obligations.Gold exports generated roughly $20 billion in revenue in 2025, nearly double the previous year, alongside solid cocoa earnings estimated at $3.9 billion in export revenue for 2025, more than double the earnings from 2024. These inflows pushed the trade balance into surplus and improved FX liquidity.

Away from Ghana, Zambia followed a similar path. The Kwacha appreciated by about 16 percent against the US dollar in 2025, trading near K22.55 per dollar by year-end. This performance placed it among Africa’s strongest currencies despite Zambia’s history of debt distress and commodity dependence. Rising copper prices were a key driver. Prices climbed to around $13,000 per tonne amid strong global demand for electrification and renewable infrastructure. Since copper accounts for more than 70 percent of Zambia’s foreign exchange earnings, higher prices translated directly into stronger inflows. Unlike previous commodity booms, however, the gains were reinforced by tighter monetary policy, progress on debt restructuring, and clearer fiscal management. These measures reduced risk premiums and improved investor sentiment, highlighting how commodity-dependent economies can still achieve currency stability when price windfalls are anchored by credible policy frameworks.

What Role Does Policy Credibility Play in Currency Stability?

Apart from commodities and export earnings, Central Bank policies played a vital role in strengthening the currency appreciation in the smaller nations that performed well. For Ghana and Zambia, government policy choices deliberately reduced uncertainty, curbed inflationary pressures, and restored confidence in monetary management. However, what distinguished these countries from their larger peers, such as Nigeria and South Africa, was not the absence of shocks, but rather how the authorities responded to them.

Ghana’s currency recovery was rooted in a sharp policy break from the past. After years of fiscal slippage and heavy central bank financing of government deficits, authorities adopted a tighter fiscal framework anchored on expenditure control and revenue mobilization. The government significantly reduced its reliance on Bank of Ghana financing, helping to slow money supply growth and ease inflationary pressure.

On the monetary side, the Bank of Ghana pursued a clearly communicated tight stance, maintaining elevated Central Bank interest rates for longer than markets initially expected. This signaled a willingness to prioritize price stability over short-term growth or political convenience. Transparent communication from the central bank, including explicit guidance on inflation targets and reserve accumulation, helped anchor expectations. Combined with an IMF-supported adjustment program, these policies restored investor confidence, attracted portfolio inflows, and reduced speculative pressure on the Cedi.

On its part, Zambia’s currency strength reflected the credibility gained from policy coordination rather than commodity prices alone. While rising copper prices provided an external boost, authorities avoided repeating past mistakes of expansionary spending during commodity booms. Fiscal policy remained restrained, with expenditure controls and improved budget transparency helping to stabilize public finances. A critical policy factor emphasized by the Zambian government was the progress on sovereign debt restructuring. By engaging creditors and advancing negotiations under the G20 Common Framework, Zambia reduced default risk and lowered its country risk premium. This improved investor sentiment and encouraged capital inflows, supporting the kwacha.

What are the Lessons Learned from Countries with High Currency Appreciation?

The experience of smaller African economies demonstrates that currency strength is less about economic size and more about policy credibility, discipline, and coordination. Countries such as Ghana and Zambia showed that when fiscal authorities and central banks align their objectives, maintain prudent financial conditions, and communicate policy direction clearly, investor confidence can recover even after periods of instability. Export earnings and commodity price increases played an important role, but they were not sufficient on their own without credible policy frameworks to anchor expectations.

For larger economies, the lesson is not that scale is a disadvantage, but that policy complexity can magnify structural imbalances and political pressures, ultimately undermining confidence. The smaller high performers illustrate that credibility compounds over time, while uncertainty erodes value regardless of economic weight. In this sense, Africa’s recent currency shifts offer a broader insight: stability is not inherited from size or resource endowment, it is built through consistent institutional choices.