Table of Contents

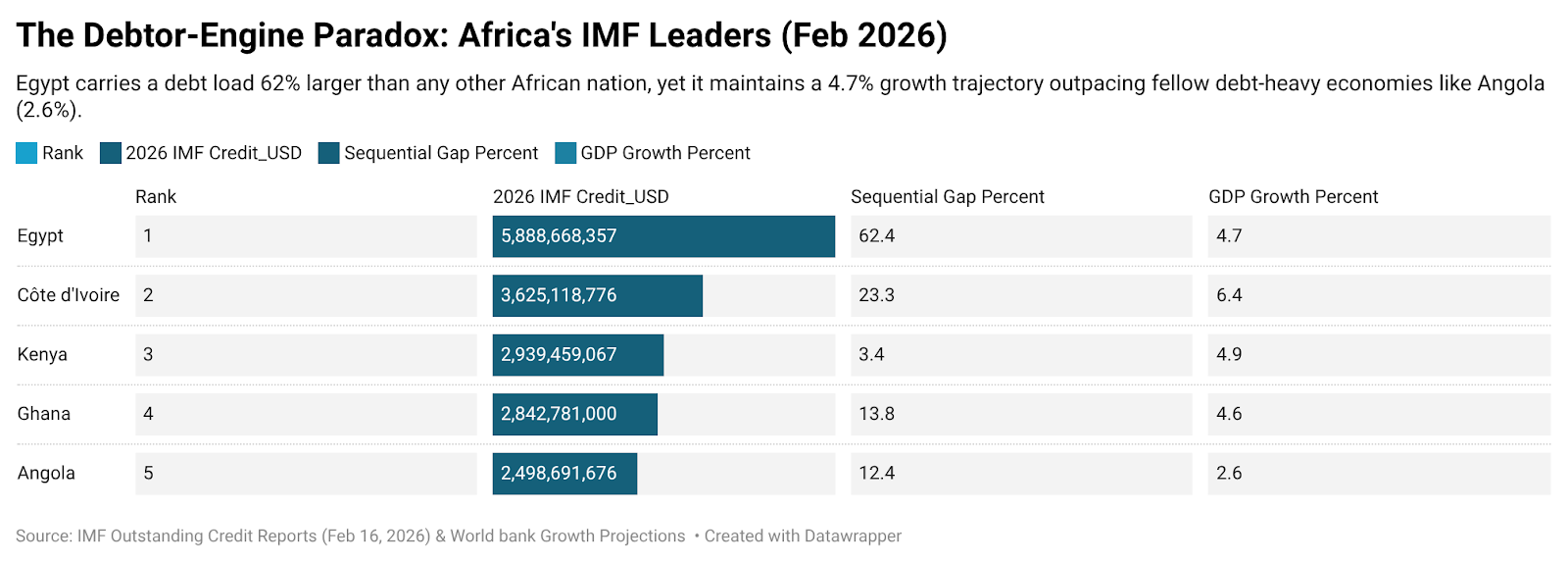

In 2026, Africa’s largest borrower from the International Monetary Fund is not facing collapse. Egypt holds the highest outstanding credit with the International Monetary Fund in Africa, with obligations exceeding 5 billion USD. No other country on the continent carries IMF exposure at this scale.

Yet, surprisingly, growth has not stalled. Egypt continues to expand at roughly 4-5 percent annually and remains the second-largest economy by GDP. Major infrastructure projects are advancing across transport corridors and energy networks that underpin the country’s long-term development strategy. Tourism, one of Egypt’s primary sources of foreign exchange and employment, has rebounded strongly after the pandemic shock.

These pillars of revenue and investment indicate an economy that has preserved operational stability even while IMF obligations have risen year after year.

In many economies, borrowing at this scale would coincide with stagnation, fiscal paralysis, or investor retreat. In Egypt’s case, debt accumulation and economic expansion have unfolded simultaneously.

How has Egypt managed to carry Africa’s largest IMF debt while sustaining growth, investment, and macroeconomic stability at the same time?

How Did Egypt Turn Africa’s Largest IMF Exposure Into a Reform Framework?

In 2016, Egypt faced macroeconomic pressures that could no longer be managed through short-term fixes. Foreign exchange reserves were under severe strain, the Egyptian pound was depreciating, fiscal deficits had widened sharply, and investor confidence was faltering. Imports were constrained, and growth risked stalling due to structural distortions in the exchange rate and subsidy systems.

Even with these pressures, Egypt needed a way to stabilize the economy and restart growth. It agreed to a $12 billion program with the International Monetary Fund, a commitment that marked a structural reset rather than a temporary bailout. The Egyptian pound was floated, ending years of exchange-rate rigidity that had distorted foreign exchange allocation. Energy subsidies were reduced, addressing a major source of fiscal leakage. Fiscal consolidation began, narrowing deficits while preserving capital expenditure for priority projects. These were not cosmetic adjustments; they reshaped the economy’s operating framework and redefined the conditions under which growth could occur.

Floating the currency aligns official and market rates, improving export competitiveness and correcting distortions in foreign exchange allocation, though it simultaneously triggered record-high inflation that tested social resilience. Subsidy reform freed public resources to fund infrastructure, power generation, and logistics corridors. Fiscal discipline strengthened budget management while allowing targeted investment to continue. Yet the question remained: how could borrowing coexist with growth? Analysis of the policy sequence shows that as IMF funds entered the country, the economy's incentive structure shifted. Manufacturers operated under realistic exchange rates, budget discipline improved, and investment flowed into sectors capable of expanding productive capacity. By 2018, industrial output and export activity were already strengthening, even as Egypt’s IMF exposure increased by billions.

Debt continued to rise because the country remained exposed to capital flow volatility, import dependence, and the financing needs of large-scale infrastructure projects. But borrowing was not simply a burden; it became a tool to reinforce stability. Data on foreign investment and project funding demonstrate that IMF engagement provided liquidity and policy oversight that reassured investors and enabled long-term planning. Crucially, this credibility paved the way for massive foreign direct investment, such as the $35 billion Ras El Hekma deal in 2024, which provided the essential hard-currency buffer needed to sustain the IMF's reform requirements. Capital inflows from Gulf sovereign funds and private investors continued to fund transport, energy, and urban development projects, reflecting confidence in the country’s fiscal and reform trajectory.

Between 2019 and 2021, Egypt accessed additional IMF facilities, including emergency support during the global pandemic. Tourism, one of the largest sources of foreign exchange and employment, collapsed globally, threatening hard-currency inflows. Instead of halting investment, authorities used IMF financing to cushion the shock and prevent systemic contraction. Hotels and travel services kept operating, supply chains remained connected, and fiscal support allowed key sectors to rebound quickly as global conditions stabilized. By the 2024–25 fiscal year, GDP growth held around 4.5 percent. As the IMF mission chief for Egypt stated, “…Growth is expected to continue strengthening, and we upgraded our forecast for FY24/25 to 3.8 percent, in light of the stronger-than-expected outturn in the first half of the year.” An IMF official further noted in 2025, “Since March 2024, the authorities have made considerable progress in stabilizing the economy and rebuilding market confidence despite a challenging external environment...”

In short, Egypt’s growth under Africa’s largest IMF exposure reflects a deliberate sequence: borrowing financed stabilization, stabilization reinforced credibility, credibility attracted investment, and investment expanded productive capacity. Debt did not suppress growth but enabled it. The country continued borrowing because each tranche reinforced liquidity, policy oversight, and confidence, creating conditions in which the economy could expand even as obligations rose.

What Does Egypt’s Debt–Growth Balance Reveal for Other Economies?

Egypt’s experience does not suggest that high debt is inherently harmful. Borrowing only suppresses growth when it is unstructured or unsupported by policy. In Egypt, IMF financing was tied to clear structural adjustments: exchange rate liberalization, subsidy rationalization, fiscal consolidation, and revenue reform. These measures were designed to correct economic imbalances rather than postpone them. Currency adjustments improved export competitiveness, energy subsidy reductions curtailed fiscal leakage, and revenue mobilization strengthened public finances.

At the same time, investment continued alongside reforms. Infrastructure expansion, energy capacity development, and logistics improvements proceeded even under fiscal tightening. This combination increased productive capacity while debt levels remained elevated. IMF projections indicate that Egypt’s debt-to-GDP ratio could decline toward roughly 72 percent by 2030 if fiscal consolidation continues as planned, showing that medium-term trajectories matter more than headline debt figures alone. However, the sustainability of this model remains contingent on reducing the massive portion of the budget currently consumed by debt interest payments and ensuring the private sector is not "crowded out" by state-led spending.

The coexistence of Africa’s largest IMF debt and sustained growth does not mean the economy is invulnerable. High external borrowing still exposes a country to exchange-rate volatility and global liquidity shifts. What Egypt demonstrates is that the impact of debt depends on strategy, credibility, and disciplined execution.

From what we have seen above, Egypt’s experience shows that high IMF debt does not signal economic weakness or inability to sustain growth. In Africa, large-scale borrowing can be a tool for supporting investment, stabilizing the economy, and enabling continued expansion, provided it is anchored by massive capital inflows and a willingness to absorb the short-term social costs of structural change. Access to IMF financing often reflects strategic policy management rather than financial distress.