Table of Contents

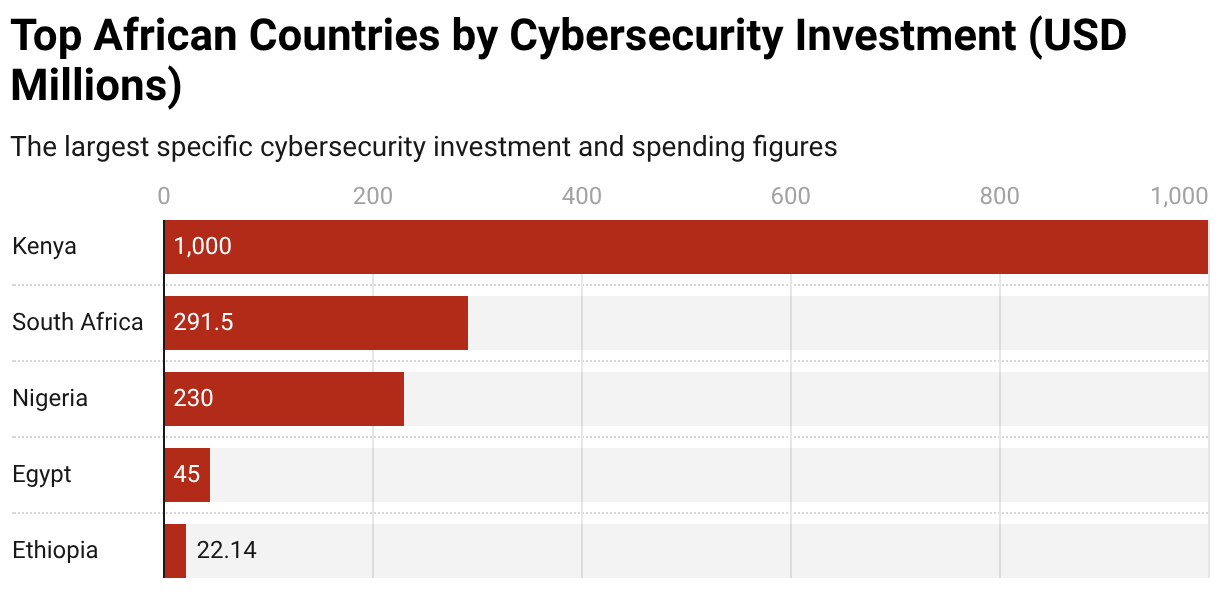

Africa’s cybersecurity market was valued at USD 0.68 billion in 2025, with that figure expected to expand to USD 0.77 billion in 2026 and more than double to USD 1.44 billion by 2031. This growth is increasingly concentrated in key markets like Kenya, Nigeria, and South Africa.

The African cybersecurity market continues to expand with a projected CAGR of 13.3% between 2026 and 2031. Investment capital continues to spread more unevenly, concentrating in a few top markets like Nigeria, Kenya, and South Africa. Investors who only look at the level of cyber threats when deciding where to invest might be missing the whole point of cybersecurity investment in Africa.

Cybersecurity dollars are moving towards markets with established, highly active and integrated digital corridors operating at massive scale. In addition, these markets have clearer regulatory frameworks and capital absorption capacity not found in secondary markets with weaker demand.

Which African Markets Are Scaling Cybersecurity Investment Fastest?

Unlike what most investors might expect, the smartest money is not going to the most attacked market or the biggest economies in the continent. It is going where cybersecurity has shifted from a defensive line item to a core economic infrastructure. In this case, East Africa is scaling fastest led by Kenya’s vibrant digital economy and reinforced by Ethiopia’s regulatory push.

Kenya, often cited as Africa’s top tech hub, sits at the center of this shift. Nairobi is the nerve-center of the new shift and has the ingredients to convert cybersecurity demand into recurring budgets. A key pillar of Kenya’s National Cybersecurity Strategy is to position the city as a regional hub. The Central Bank of Kenya has played its part by mandating that licensed banks integrate advanced fraud-detection systems into their core operations. With over 100 million mobile-money transactions happening every month, there is a huge need for security measures like fraud prevention and identity verification. A massive $1 billion digital ecosystem project by Microsoft-G42 is boosting this effort by creating a secure cloud region in East Africa and training people in cybersecurity.This shows that the smartest investors focus on places where risk is managed by guaranteed demand for security, driven by big projects and favorable regulation.

Ethiopia further strengthens the case for East Africa as a fast-scaling market from a different angle. The country is not yet a juggernaut of cybersecurity on the continent, but an emerging data point tells a revealing story that most investors might be missing: In 2025, banks in Ethiopia spent 35% more on cybersecurity. This happened after the central bank started requiring regular security tests. Now, bank budgets for cybersecurity in Ethiopia are growing much faster, at about 2.6 times the rest of Africa’s CAGR. The main idea is bigger than just Ethiopia. Across Africa, new rules are doing more than just creating paperwork. In specific countries, these rules are immediately forcing companies to buy security products. For security vendors, this is a much more reliable sales pipeline than trying to raise awareness or talking about digital transformations.

Nigeria shows what happens when companies are forced to spend on security because of new rules and regulations. Laws like the Nigeria Data Protection Act, the GAID implementation regime, mandatory NDPC registration, annual audits, 72-hour breach notification and strict oversight from the central bank now require companies to register, perform annual audits, and report data breaches as soon as they occur. Huge fines against companies like Multichoice (NGN 766.2 million) and Meta (USD 220 million) prove that breaking these rules is costly to those companies. In 2025, over 1,300 organizations in finance and gaming were investigated, showing that the government is serious about enforcement. While spending is increasing, Nigeria still ranks lower in global cybersecurity indexes and is currently placed in Tier 3 in the ITU Global Cybersecurity Index. This means most of the money is being spent to catch up with basic standards rather than investing in new, advanced cyber technology.

South Africa presents a mixed bag when it comes to cybersecurity. It has high enterprise demand and major investments from tech giants like Google and Microsoft. The government has put in place strong regulations like the Cybercrimes Act, POPIA, and the South African Reserve Bank’s resilience requirements which help keep data safe. Despite these obvious strengths, the country still suffers from a barrage of cybercrime attacks. Organizations have to avert over 1,800 attacks every week. In 2025, telecom fraud and cyber attacks cost the country ZAR 5.3 billion, and bank account thefts added another ZAR 1.8 billion in 2024 from over 100,000 bank-account attacks. These total losses of ZAR 7.1 billion are about 31% higher than the ZAR 5.4 billion Microsoft committed to spending on cloud technology and training. These figures show that even though South Africa is a big market, the cost of cybercrime is still growing faster than the money being spent to stop it. This makes it the clearest example of underinvestment relative to exposure.

What's Driving The Divergence In Spending?

The difference in how much countries spend on cybersecurity comes down to new laws and regulations, the growth of digital finance, and the build-out of new cloud infrastructure and systems. However, these changes are happening at different speeds in different markets. In Kenya and Ethiopia, spending is growing fast because cybersecurity is now a key part of their economic growth plan. For example, Kenya needs more security because many people use mobile money, and the central bank now requires banks to have systems that find fraud. Also, the cloud project by Microsoft and G42 is creating a strong foundation. This combination of high demand, government support, and new technology makes Kenya a great place for cybersecurity companies and investors. In Ethiopia, banks also started spending much more on protection after the central bank required them to perform regular security tests.

What Does The Spend-To-Risk Ratio Really Reveal?

The amount of money spent on security compared to the risk shows that Africa is dangerously underinvesting. This is especially clear when you consider that 10% of the continent's total economic production (GDP) is lost to cyberattacks every year. Africa is expected to add only about $670 million in annual cybersecurity market value between 2026 and 2031. However, the continent has already suffered more than $3 billion in total cyber incident losses between 2019 and 2025. In other words, market growth is real, but it is still meager compared to the scale of harm. That is why the most attractive cyber markets are not simply the ones spending the most today. They are the ones where spending is becoming structurally unavoidable.

When we look at specific industries, the Banking, Financial Services, and Insurance (BFSI) sector still buys the most cybersecurity products, making up 25.2% of the market.This is not unusual given how many rules banks have to adhere to and how often they face fraud. However, the really exciting news is that healthcare is expected to grow the fastest at a 15.1% annual rate (CAGR).This suggests that future cybersecurity growth won't just come from banks and phone companies (telcos). Instead, it will come from sectors like healthcare that are putting sensitive patient information online but don't yet have the strong security systems that the finance industry does. Investors searching for the next big winner should focus on tools for server and system protection, identity access, and fraud detection that can first be sold to financial technology (fintech) companies and then expand into healthcare systems and public digital services.

The ITU rankings show a clearer picture of what’s going on in the continent. Seven African countries including Kenya, Mauritius, Tanzania, Ghana, Egypt, Rwanda, and Morocco have made it into Tier 1 of the 2024 Global Cybersecurity Index. Meanwhile, South Africa is holding its own in Tier 2, while Nigeria and Uganda are still in Tier 3. Still, more than half of the countries on the continent score below the global average. This shows us that Africa isn't just one giant market; it’s more like three distinct tiers: the advanced hubs with established policies, the growing markets that are starting to enforce rules, and a long list of countries that aren't quite ready yet, where digital growth is moving way faster than cybersecurity readiness. For anyone looking to invest, this isn’t a reason to stay away or have second thoughts. Instead, it’s a roadmap showing exactly where premium services, channel partnerships and category leadership are going to appear first.

Where Should Strategic Investors And Cybersecurity Vendors Direct Their Focus?

The takeaway message for investors and security companies is simple. If you want to grow quickly and scale right now, focus on South Africa and Nigeria. In these countries, high numbers of attacks, large fines, and fraud are forcing companies to spend money on security immediately. However, if you want the smartest long-term growth, look toward East Africa, especially Kenya. This region is strong because it has many digital finance companies, local cloud services, and government policies that support tech growth. The best strategy is not just to fix current security problems, but to invest in markets where cybersecurity is built into the very foundation of the digital economy.

{kind=link}