Table of Contents

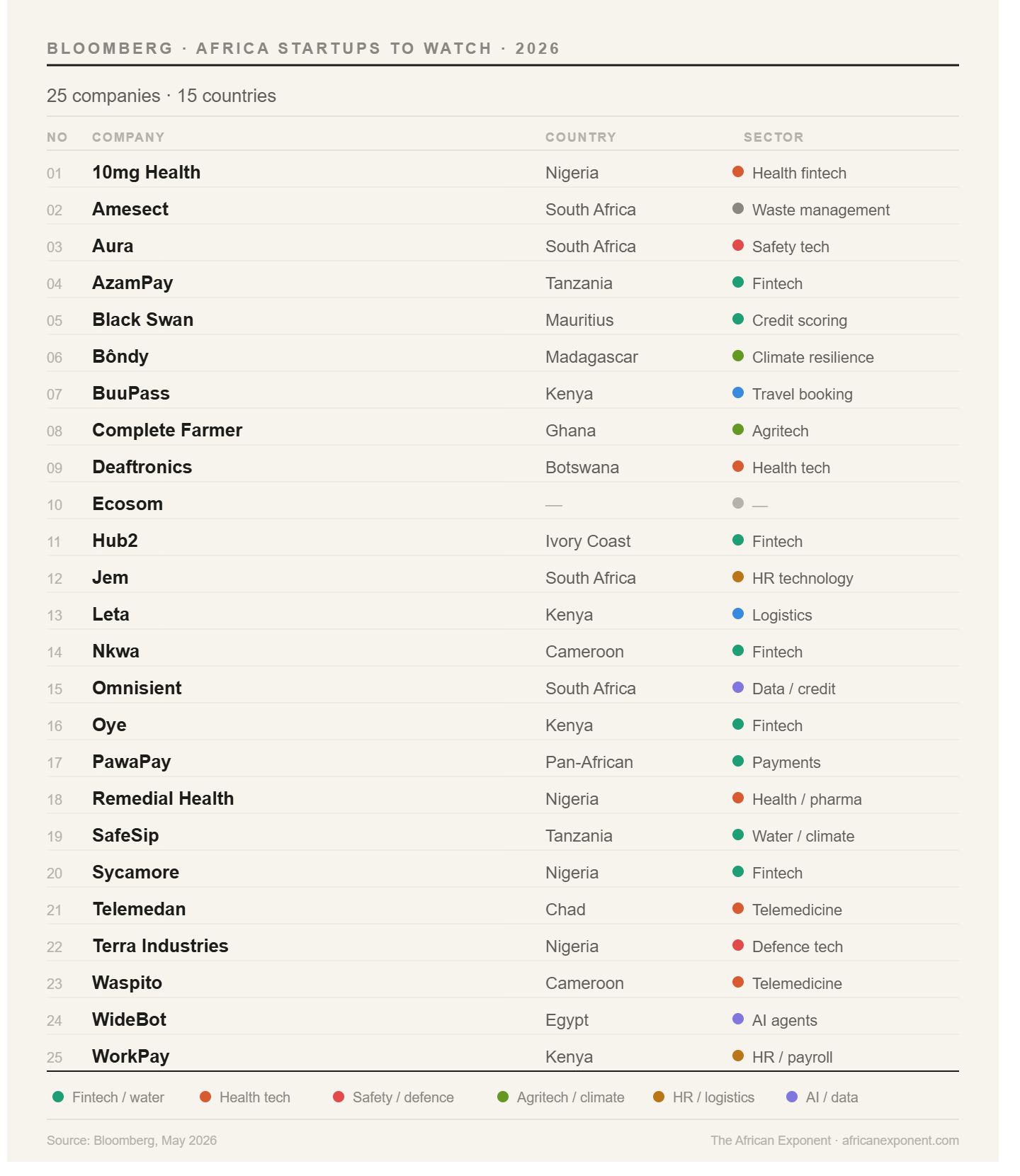

One in four dollars of global mobile-money transactions flows through West Africa, according to the GSM Association. That single fact explains why Africa's founders and investors keep returning to the same territory. Of the 25 African companies on Bloomberg's 2026 watchlist, fintech claims the largest share — and the reason is straightforward: the continent's financial infrastructure remains broken in ways that create genuine commercial cases, not merely venture-capital narratives. As the African Exponent's own survey of 45 fintech startups showed earlier this year, the sector spans everything from payroll lending to insurance, yet its core problem remains the same: millions of Africans and their businesses are invisible to formal credit systems.

Small businesses cannot borrow without formal credit histories. Black Swan, a Mauritius-registered fintech co-founded by Tanzanian entrepreneur Derick Kazimoto, attacks that problem by analysing mobile-money transactions, utility bill payments and other alternative data to assess creditworthiness. The startup won the MEST Africa Challenge 2025, securing $50,000 in equity and access to Absa's commercial networks across the continent. South Africa's Omnisient takes a related approach: its platform has already helped banks assess more than 8 million previously unscorable consumers, with 3.2 million qualifying for credit who would otherwise have been declined. Hub2, founded in Ivory Coast in 2017 by Ashley Gauzere, a former Orange executive, connects mobile-money wallets, bank accounts and digital wallets on a single platform, targeting the fragmented payments landscape of the CFA franc zones. Sycamore, a Nigerian digital lender founded by Babatunde Akin-Moses in 2019, has expanded to the United Kingdom to serve Africans abroad — a reminder that the diaspora remittance corridor, one of Africa's most contested financial battlegrounds, remains an open prize.

What unites the best of these companies is unglamorous precision. They are building underwriting models in markets where formal income data barely exists, and constructing payment rails specific to regulatory environments that global platforms have largely ignored. That is harder than building a consumer app, and considerably harder to replicate.

The danger lies elsewhere. Lending punishes growth without discipline. Sycamore's own backers have acknowledged the tension between expansion and risk pricing, and they are right to name it plainly. If African digital lenders repeat the mistakes of the global lending boom, disbursing fast and collecting slowly, the current funding enthusiasm will not survive the first serious credit cycle. Equity's share of fintech funding across Africa already fell from 60% to 32% between 2024 and 2025, according to Briter Bridges, as investors grew more selective.

Health finance sits at the most durable edge of this wave. Remedial Health, a Nigerian startup, works with more than 45,000 providers and says it has financed over $50 million of medicine — a classic embedded finance play built on supply-chain relationships that are sticky in ways consumer credit is not. Then there is 10mg Health, founded by pharmacist Christian Nwachukwu in 2022, which finances hospital and pharmacy bills through its 10mgCredit product, betting it can price medical risk better than traditional lenders.

The list's two most arresting outliers are not fintechs at all. Terra Industries, a Nigerian defence-technology startup founded in 2024 by Nathan Nwachuku, 22, and Maxwell Maduka, 24, has raised $34 million from investors including Joe Lonsdale's 8VC and Lux Capital to build autonomous surveillance systems protecting critical infrastructure. Telemedan, from Chad, deploys solar-powered telemedicine kiosks equipped with diagnostic tools, connecting patients in off-grid areas to remote doctors. It has served over 60,000 patients. Both companies exist because states have failed to provide basic security or healthcare. That is a brutal market condition — and, for now, a durable one.

Whether the fintech cohort justifies its prominence will depend less on technology than on credit discipline, investor patience and regulatory coherence across dozens of jurisdictions. The opportunity is real. So is the distance between a compelling pitch and a profitable business.